Dear Chuck,

I’m grateful that my parents prepared for aging in place and for assisted living, if necessary.

Some of my friends’ parents have not, and the financial pressure within those families has been difficult to watch. What tips can you offer people so they can avoid this financial drain in their senior years?

Getting Ready for Getting Old

Dear Getting Ready for Getting Old,

Your parents will be remembered for their consideration and wisdom. Hopefully, your question can inspire many other families to “set their house in order” (Isaiah 38:1) to be ready for the financial burden of aging and leaving our earthly home.

A Serious Financial Shock

It is a fact that many of America’s elderly cannot cover their overhead. The National Council on Aging reports that 45% of older adult households do not have the income needed to cover basic living costs based on cost-of-living data from the Elder Index. 80% are unable to cover a shock like widowhood, serious illness, or long-term care. In addition, Investopedia gathered data showing that three in ten Americans in their 50s have no retirement account or pension. This is a sad reality.

While the parents of your friends may appear as if they have nothing, it is possible they have lived sacrificially to prepare. Possibly, they have life insurance and invest in assets that children are unaware of. That’s why it’s important to discuss the matter if possible. Unfortunately, not all families have the luxury of transparency due to relationship challenges, mental health, or other issues with children and/or blended-family situations.

Getting Ready for the Inevitable

Preparing financially for one’s senior years is one of the most important forms of stewardship. It’s not just about having enough money. It’s about creating stability, preserving dignity, and living with purpose. The key is to begin now, long before becoming senior citizens. There is no escaping it. Should the Lord will it, we will become senior citizens ourselves one day! Start now by taking the following steps:

The earlier you begin, the better. Time is a powerful factor in financial preparation because of compounding. Consistently saving and investing over decades allows even small contributions to grow significantly. Even if starting late, intentional planning can make a meaningful difference.

A Simple Plan to Follow

A foundational step is to build and maintain retirement savings. Contributing regularly to 401(k) accounts or IRAs provides long-term growth and potential tax advantages. If employers offer a match, take full advantage of that benefit. It’s one of the most effective ways to accelerate savings.

Reduce and eliminate debt. Entering retirement with large financial obligations can limit flexibility and increase stress. Aim to free up income so that resources will support needs rather than cover past decisions.

Plan for healthcare costs. Medical expenses typically increase with age and can become one of the largest financial burdens in retirement. Understanding insurance options, setting aside savings, and considering long-term care needs are all part of wise preparation.

Create a sustainable income strategy. This includes Social Security, retirement accounts, and any additional income sources. A clear plan helps ensure that your money lasts.

Fund an emergency account. Unexpected expenses still arise in old age. Accessible savings prevents the need to rely on debt or having to withdraw from long-term investments at an inopportune time.

Make lifestyle decisions. Living below your means before and during retirement creates margin and reduces financial pressure. It may also open the door to greater generosity and the freedom to act on what God lays on your heart.

Seek wise counsel. Financial advisors, trusted mentors, and knowledgeable friends provide perspective and help avoid costly mistakes. Proverbs reminds us that wise plans succeed with many counselors.

If possible, plan to continue working or pursuing meaningful activity to provide both income and purpose. View retirement as a season of contribution in new ways.

Anchor your preparation with trust. Financial planning is essential, but it does not provide ultimate security. God is the Provider. Preparation is an act of stewardship that must be paired with faith in God, who numbers our days.

The Bible teaches that the way we handle money now impacts our future both here and into eternity. We need not prepare out of fear but out of faithful stewardship. Here are financial actions and attitudes that are supported by Scripture:

Financial preparation for senior years is more than accumulating resources. It’s about building a life characterized by wisdom, discipline, and purpose. When that season comes, you are not defined by financial stress but by a life that is filled with peace, generosity, and impact. Hopefully, younger family members can serve you without the stress of wondering how to pay for your care.

More Resources

Financial Literacy Declines in Older Adults

Gen X Facing a Retirement Crisis

Preparing for Retirement Involves More than Finances

Crown offers many biblically based, practical, and empowering courses and studies to help families find freedom with their finances. Learn how to be a faithful financial steward of the resources God provides.

This article was originally published on The Christian Post on May 22, 2026.

Dear Chuck,

My grandfather is giving me $5,000 for my college graduation that he wants me to invest. He says too many people wait until they think they can afford to invest, but starting young is crucial. He is giving me freedom to pick stocks or funds but expects to see proof.

Young Investor

Dear Young Investor,

Congratulations on your graduation! You have a wise grandfather!

Most people wait until they think they can afford to invest before they begin. Your grandfather knows that the earlier you begin investing, the longer your money has to grow.

Quick Guidelines for Investors

I want to share some Biblical principles and expert insights to help you become a better investor; however, let me frame my comments with some important perspective first:

What the Bible Says

God’s Word offers distinct principles for guidance in growing and managing resources.

Lessons from Warren Buffett

For years, I have read books and articles by one of the greatest investors of our time, Warren Buffett. I recommend that you read books by Benjamin Graham and Warren Buffett to learn from their years of investing expertise. Here are some key takeaways:

Extra Insights from the Experts

Be Prudent and Diligent

Investing is anchored in wise, patient, and purpose-driven stewardship—growing what we’ve been given while keeping our trust anchored in God, not money. Investing places our money at risk of loss. Be prepared for losses and to ride out dips in the economy. The longer you are able to remain invested, the better the likely performance. No one can avoid losses; no one can time the market’s fluctuations. Just be diligent.

“Lazy hands make for poverty, but diligent hands bring wealth.”

Proverbs 10:4 (NIV)

“The plans of the diligent lead surely to abundance, but everyone who is hasty comes only to poverty.”

Proverbs 21:5 (ESV)

“In all toil there is profit, but mere talk tends only to poverty.”

Proverbs 14:23 (ESV)

Do you want more tools and tips on financial stewardship? Are you interested in receiving encouraging ministry updates from around the world? Sign up to receive the Crown Newsletter emails by using the form on the homepage at Crown.org.

This article was originally published in The Christian Post on May 15, 2026.

Dear Chuck,

I maxed out our credit card for some unexpected home repairs, including a new HVAC. The interest rate is ridiculously high since I did not pay it off last month. I’m considering using a HELOC to pay off the credit card. Is that a good idea?

Worried About My Credit Card Balance

Dear Worried About My Credit Card Balance,

My first reaction whenever someone tells me that they are planning to use debt to pay off debt is to say, “You are tap-dancing on hot coals.” Moving short-term debt to long-term debt to lower the interest rate or the monthly payments may be necessary for the relief you seek, but at some point, you can get really burned.

It would be helpful to have a full conversation to understand your overall picture. I don’t want to presume anything about your circumstances, but the next questions I would ask are:

A Better Way

If credit card payments are becoming difficult or you want to lower the interest you’re paying each month, here are several steps and options that may help:

HELOCs – The Good and the Bad

Only consider a home equity line of credit (HELOC) if you have a significant amount of home equity, are disciplined in your spending, and have a secure source of income. Be sure you can check all the boxes I just listed.

While helpful in lowering borrowing costs, they come with risks. They have variable rates and are secured by your home. Missed payments can endanger home ownership. This kind of loan requires time, paperwork, possibly an appraisal, an origination fee, and closing costs from 2–5% of the loan amount. Other fees may be charged for a credit report, a notary, and a title search. These can easily cost several thousand dollars, depending on the desired line of credit. If you decide to apply for one, make sure you have a repayment plan in place.

The amount you can borrow is determined by your credit score, debt, income, mortgage payment history, and home equity. If you sell your home before paying off the HELOC, proceeds from the sale will be used to close out the debt. Only go with a legitimate lender. Research customer reviews, ratings, and any regulatory action or lawsuits against the company. Applications received online or in the mail that you did not request are most likely scams.

If you itemize deductions on your tax return, any interest from a HELOC that is used to buy, build, or substantially improve your primary residence or a qualified second residence is tax-deductible up to certain limits. Clear documentation is required: renovation contracts, itemized receipts, invoices, and bank statements showing payments to contractors that prove the use of funds.

Pros

Cons

On April 27th, Bankrate reported that interest rates on a $30,000 HELOC dropped to 7.81%. That is the lowest level seen in two years among their national survey of lenders.

The diagram below can help you consider all of the options and make a wise choice on how to pay off this credit card debt.

| OPTION | RATE RANGE | HOME AT RISK? | CREDIT REQUIRED | BEST FOR |

| HELOC | 7–10% | Yes | 680+ | High equity homeowners, large balances |

| Home Equity Loan | 7.5–10.5% | Yes | 680+ | Those wanting fixed-rate certainty |

| Balance Transfer Card | 0% intro, 18%+ after | No | 700+ | Small balances, 12–18 month payoff |

| Personal Loan | 10–18% | No | 650+ | No home equity, moderate balances |

| 401(k) Loan | Prime + 1% | No | N/A | Employed borrowers, small amounts |

| Debt Management Plan | No new debt | No | Any | Struggling with minimums, needs structure |

Financial Slave

The Bible never declares that debt is sin. However, Proverbs 22:7 says, “The borrower is servant to the lender.” I don’t want you trapped in a never-ending cycle, juggling the weight and stress of your debt. Choose the best path forward, and seek to avoid any new consumer debt in the future.

Extra Reading

Consider reaching out to Christian Credit Counselors. They are a trusted partner of Crown and can help you create a debt management plan tailored to your current needs—putting you on a path toward financial freedom.

This article was originally published on The Christian Post on May 8, 2026.

Dear Chuck,

I know all the steps to financial health. I’m just experiencing extreme frustration because of such slow progress. We were making headway until the price of gasoline jumped; now everything seems to be falling apart. I’m tempted to just trash the family budget completely and do the best I can month to month.

Trash the Budget

Dear Trash the Budget,

I hear your pain. Many others are experiencing your frustration and financial stress. I was recently reading an article about how we all tend to deal with stress differently, so I created a framework that may be helpful to you.

When facing a circumstance in our life that causes stress, we tend to deal with it in a variety of ways:

Stress Out – This is when we succumb to fear, anxiety, or even depression, and we enter the doom loop. We tell ourselves that things are bad and will only get worse. We lose hope, become exhausted, and want to give up.

Drop Out – This is an attempt to deny the problem by ignoring it. We avoid facing the problem in hopes it will go away.

Fake Out – This is pretending all is well by masking the stress with other activities that soothe our nerves. This attempt leads to addictions and foolish wastes of time without addressing the real issue. Think: endless scrolling, mindless games, binge-watching movies, and addictions.

Cry Out – This is when we recognize the problem is bigger than we can handle and invite God to help us. When we cast our cares upon the Lord, we acknowledge we are weak and need Him.

Let me offer a Biblical approach to your stress: Face the Battle, Take Action, and Don’t Give Up.

Face the Battle Head-On

Every believer has the responsibility of wisely managing resources. That can be difficult in the midst of inflation, economic uncertainty, and business, family, or personal challenges. This responsibility can create serious stress, even despair, just as you are describing. We can learn to confront these financial challenges with confidence by declaring war and not giving up! It boils down to imagining yourself as a soldier on the battlefield so you can stand up under stress and discouragement, knowing that God will help you through it one day at a time.

Finally, be strong in the Lord and in the strength of his might. Put on the whole armor of God, that you may be able to stand against the schemes of the devil. For we do not wrestle against flesh and blood, but against the rulers, against the authorities, against the cosmic powers over this present darkness, against the spiritual forces of evil in the heavenly places. Therefore take up the whole armor of God, that you may be able to withstand in the evil day, and having done all, to stand firm.

Ephesians 6:10–13 ESV

Refuse to allow the enemy to accuse, shame, or remind you of failure. Satan will attack whether we are weak and vulnerable or proud and ungrateful. Just remember, the Victor is on your side, and you need to trust Him by walking in His ways.

Now Take Action

That budget is actually your friend. You simply need to make adjustments every day that keep you on track to live beneath your means.

In all toil there is profit, but mere talk tends only to poverty.

Proverbs 14:23 ESV

Imagine hiking a mountain. You follow a deeply wooded trail, winding your way back and forth over a path that seemingly leads to nowhere. The terrain becomes so treacherous that you have to pause to catch your breath before moving on. Determined to make it to the top, you trudge on; suddenly, there’s a clearing. You look behind you, able to see just how far you have come. Small steps can lead to breakthroughs, but we have to keep going.

Nothing of value comes easily. God wants you to depend on Him for strength and provision. It is humbling but precious to experience His amazing grace as we implement the principles He gave us for our good. It is only when we recognize our limits that we can begin to see His limitless power, might, majesty, faithfulness, and wisdom.

Delight in the simple knowledge that you are willing to climb your way out of this pit. I applaud your effort!

You admit that you know the steps, but let me remind you of the importance of the following:

Never Give Up

Focus on what you can control. Don’t expect perfection of yourself or others. Turn grumbling into praise by looking for God’s goodness and giving thanks in everything. You may encounter times when you don’t make progress. Rejoice that you are not going backward.

Sacrifice and hard work are satisfying in the long run. They are good for us because they build character and produce hope. As the Apostle Paul wrote in Romans 5:3–5, “We rejoice in our sufferings, knowing that suffering produces endurance, and endurance produces character, and character produces hope, and hope does not put us to shame, because God’s love has been poured into our hearts through the Holy Spirit who has been given to us” (ESV).

God Will Give You Strength

Do not be afraid. Trust Him.

Fear not, for I am with you; be not dismayed, for I am your God;

I will strengthen you, I will help you, I will uphold you with my righteous right hand.

Isaiah 41:10 ESV

But they who wait for the Lord shall renew their strength; they shall mount up with wings like eagles; they shall run and not be weary; they shall walk and not faint.

Isaiah 40:31 ESV

What Is Rewarded Is Repeated

Be faithful with little by prioritizing what is truly valuable. As you make progress, plan for small celebrations when you reach a new savings or giving goal. By taking small steps, you will create a new discipline that will pay long-term, even eternal, rewards.

Crown has many biblically based, practical, and empowering courses and studies that can help you find freedom with your finances. Learn how to be a faithful financial steward of the resources God provides.

This article was originally published on The Christian Post on May 1, 2026.

Dear Chuck,

I’m in my 40s and have put off saving for retirement. My current job offers an employer-matched 401(k), and I’ve been advised that it’s foolish not to participate. I’m afraid to make automatic deductions in case money gets too tight. Should I do it anyway?

Contribute to My 401(k)

Dear Contribute to my 401(k),

It would certainly be helpful to understand the full picture of your financial situation. While I hesitate to give blanket financial advice, it is hard to go wrong using the benefits of an employer-matched retirement account! There are a few precautions that I will get to below.

Contributing to a retirement account is a privilege for us—one that our forefathers could not have imagined. Saving for the future is one of the most important financial habits, and it is taught by Solomon in the book of Proverbs:

“The wise man saves for the future, but the foolish man spends whatever he gets.”

Proverbs 21:20 TLB

A Few Precautions

Before socking away money for the long term, be sure two things are in place:

With these two financial goals in place, you are able to eliminate the fear you expressed about “money getting tight.” These two achievements establish the freedom to put money away for the long term without the worry of having to pay a penalty for early withdrawal.

First, Look at the Ant

Learning to save for short- and long-term needs does not happen by accident! It happens through intentional choices made day after day after day. Like any other habit, it is built over time through consistency and sacrifice. So how do you develop the habit?

“Go to the ant, you sluggard; consider its ways and be wise! It has no commander, no overseer or ruler, yet it stores its provisions in summer and gathers its food at harvest.”

Proverbs 6:6–8 NIV

This verse is a bit comical if you stop to think about it; the message should be clear that even though an ant is a tiny creature with a nearly microscopic-sized brain, it is an example of great wisdom! Why? Because it stores provisions for the future. The point is that we should be just as wise as one with such a tiny brain!

Next, Get Going!

The sooner you start using your 401(k), the better—no matter how small. Just start. Begin with something manageable, even if it’s just a small percentage of your income. With consistency, you will develop the habit and probably never miss the money. Saving becomes an extension of how you live: sacrificing current wants for future needs.

Automate your savings. Setting up contributions to occur automatically removes the temptation to spend what should be saved. This is a very important step because when the money is not available to spend, you learn to do without. The structure strengthens the discipline. For some, it helps to consider the money locked away, never to be touched until retirement age—but also to be celebrated when you achieve a milestone goal.

Unite saving with your purpose. Retirement saving is preparing you—and if you are married, your spouse—with the freedom to live, give, and serve without financial pressure later in life. Connecting the importance of saving to a bigger life purpose will keep you motivated to stay the course and allow the freedom to obey God’s call on your life.

Saving Requires Sacrifice

Saving consistently, for the majority of people, means having to make sacrifices. Here are a few suggestions:

Choose to be grateful and content by protecting your mind and taking your thoughts captive. Adopt the mindset of choosing long-term peace over short-term pleasure. Every dollar you set aside today builds margin for tomorrow. Over time, the compound interest earned on small, faithful decisions leads to freedom, stability, and the ability to finish well. Just as there is a cost to saving, there’s a greater cost to not saving.

Opting Out Has Ramifications

Pausing automatic deductions to retirement accounts is costly. It should be a last-resort decision. After exhausting all other options, you may have to temporarily halt contributions. Consider the pause a life preserver—only use this option to make it safely to shore. Passing on an employer-matched 401(k) means losing free money and the tax benefits that come with it.

Valid reasons to pause:

Ill-advised reasons to pause:

Encourage Your Children to Save

Once you get your plan in place, you are now setting a great example for others in your life. If you have children, I encourage you to teach them to start now. It helps to reward their efforts. Consider matching their deposits up to a certain dollar amount. Build interest and excitement by watching it compound over time.

Our children were taught to allocate all income they received from gifts or odd jobs into three categories: Giving, Saving, and Spending. Today, I would add a fourth: Investing. The younger they are, the higher the percentage that is kept in savings. The older they get, the more of their income they can spend, but they should always save 10–20%.

Small, Consistent Steps = Big Impact

Remember: It is better to sacrifice comfort today for security tomorrow. Consistency counts. Just get started, and don’t look back. If consumer debt is eating up your ability to put money away, get help to eliminate it as quickly as possible while also saving for the short and long term.

As an additional resource, read Kiplinger: “This is What You’re Really Losing if You Cut Back on Your 401(k) Contributions.”

If credit card debt is holding you back from saving, reach out to Christian Credit Counselors. They are a trusted partner of Crown and are able to help consolidate debt and get one on the road to financial freedom.

This article was originally published on The Christian Post on April 24 2026.

Dear Chuck,

We were hoping to take a vacation this year, but we really can’t afford it. Any ideas on ways I can avoid disappointing the family?

Vacation on a Limited Budget

Dear Vacation on a Limited Budget,

The Bible records that God rested from His work. If He needed to rest, we certainly do too! We should plan to periodically take time off to rest and reset our minds and bodies. But going into debt or creating financial stress to take a vacation is not wise.

Several years ago, I addressed the importance of vacations. They are Biblical and can be taken without incurring debt. Many people are in the same straits as you. Emily Stewart at Business Insider says, “It’s a complicated moment for travel planning… When a lot about the world feels uncertain, there’s a comforting level of security in sticking close to home.”

Staycations Can Be Fun

If you have not considered staying at home for your vacation, “staycations” are actually booming across the country. Many people are tired of staged vacations and tourist traps and yearn for authenticity. Rising airfare, costly hotels, and airport turmoil are several reasons to find ways to enjoy being near home.

Some benefits of staycations include:

This concept focuses on enjoying local activities and attractions without spending the night away. Imagine your home as a destination spot, and build out your agenda from there. You can discover parks, museums, historical sites, festivals, and more, usually within a short drive from your home. Take in farmers’ markets, theatres, art galleries, and sporting events. Convenient and cost-effective, staycations give you complete flexibility and the opportunity to experience your community, county, and state in a fresh new way.

Now that our sons are grown, my wife and I often use vacation time this way. We complete projects around the house, go hiking or antique shopping, or stay overnight in the mountains just a few hours away. Some people enjoy camping or staying at a nearby cabin, hotel, or VRBO. They can afford it and find it just as fun as leaving town without the headache of driving a long distance, flying, renting a car, etc.

Affordable Vacation Ideas

Through the years, we discovered affordable activities to do with our four sons. We fished, played tennis, and invested in yard games we could do together. Croquet, frisbee, disc golf, bocce ball, and whiffle ball are still popular entertainment with the boys and their families. We’ve found that the most important part of the time off work is being with those you love. Entertainment can be minimal.

Finding a way to spend time outdoors is important. If you have children, discover local, state, and national parks near you. If you have a home, consider setting up fun games like “bucket golf,” disc golf, or an obstacle course to surprise your children.

Sometimes the weather doesn’t cooperate. This is when a collection of board games is handy. We have fun memories of Monopoly extending for days—even after the boys got married. Read great books, enjoy a classic movie, and cook together.

Find some more great staycation ideas here. An article at Travel and Tour World also provides interesting data.

Destination Vacations Can Be Fun—but Costly!

Some people love the adventure and thrill of traveling. The break from routine allows them to recharge. Those who travel to the same place year after year build memories of tradition. The annual trips create deep family bonds.

However, there are some downsides to consider:

Make a Plan, and Be Cautious

A vacation takes planning. If you decide to go this route, beware of third-party scams! Sarah Hopkins at AAA says, “According to the American Hotel and Lodging Association, 23% of consumers said they were misled by third-party booking sites on the phone or on the web, translating to more than $5.7 billion in online booking scams. Customers are led to believe that they are booking through an official hotel or airline site, but they’re actually doing business with a third-party middleman. This can lead to lost reservations, incorrect accommodations, undisclosed fees, or worse.”

A deal pops up online showing discounted flights, a beautiful rental, or a hotel at a price that’s too good to ignore. You click, book, and pay and then discover you’ve been scammed.

So how can you protect yourself?

First, book directly with the airline, hotel, or official rental website. Third-party sites can be legitimate, but they’re also where many scammers hide. Going straight to the source reduces your risk. Second, be cautious of prices that seem unusually low. Scammers use urgency and deep discounts to get quick decisions. If it feels too good to be true, pause and check before you commit. Third, verify the listing, and use secure payment methods. Double-check property listings. Sometimes scammers copy photos from legitimate sites. Avoid wiring money or using debit cards or payment apps when booking a reservation. I recommend using a credit card because of the protection it offers. Some extra diligence now can save you from a lot of stress later.

Create Memories, Not Debt

It’s important to reorient our hearts and minds to what really matters. Rest during time off prepares us to work as unto the Lord, no matter our vocation. So whatever you decide to do, create great memories, not financial headaches.

If credit card debt is a financial burden for your family, reach out to Christian Credit Counselors. They are a trusted partner of Crown and are able to help consolidate debt and get one on the road to financial freedom.

This article was originally published on The Christian Post on April 17, 2026.

Dear Chuck,

I’m what you’d call a “soccer mom.” We have three kids, and I feel like I run a taxi service for all their sports. Our health insurance is going up, gasoline prices are up, and groceries are killing our budget. I doubt we can afford a bigger house now that interest rates are high. How do good stewards deal with all of this at once?

Overwhelmed With Family Expenses

Dear Overwhelmed With Family Expenses,

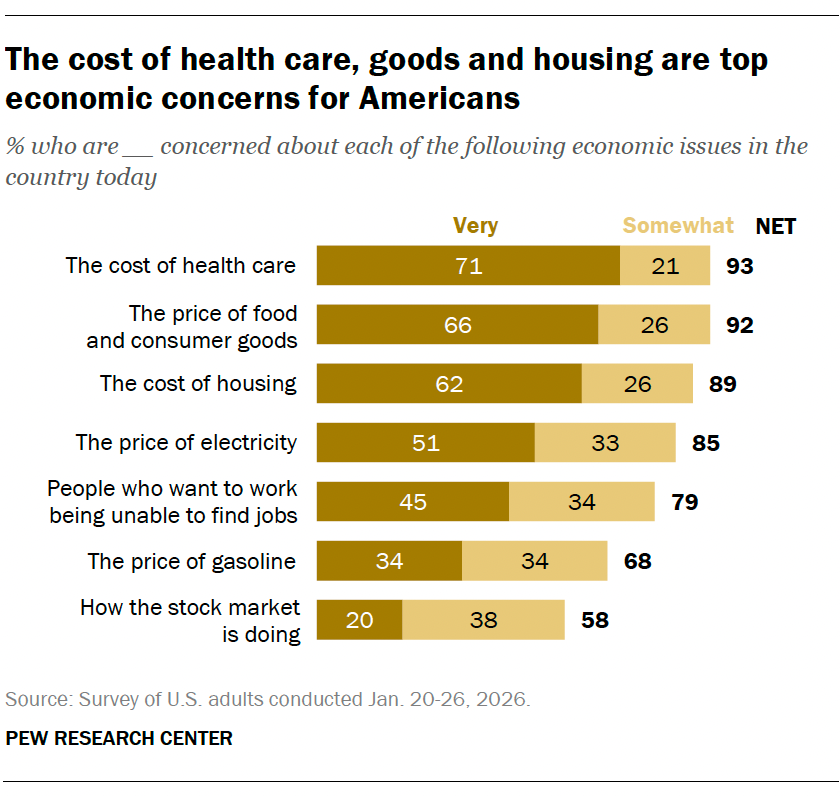

That is a lot of concern packed into a small paragraph! Whether you are a “soccer mom” or a “dual-income no-kids family” (DINK), many Americans are feeling the same financial pinch. Let’s look at the big picture and then narrow it down to some of your specific areas of pain.

Widespread Economic Concerns

Most Americans have negative views of the U.S. economy right now. According to Pew Research, “About three-in-ten U.S. adults (28%) rate economic conditions in the country as excellent or good, while roughly seven-in-ten (72%) rate them as only fair or poor.”

Experts Agree

Sarah Foster at Bankrate says, “The massive post-pandemic price burst hasn’t just challenged consumers’ ability to afford the items they want and need. It’s also damaged their personal finances, making it harder for consumers to take the prudent financial steps that could set them up for success in the long run… Those steps include saving for emergencies, investing in retirement, and covering expenses without incurring credit card debt.”

Taryn Phaneuf at Nerdwallet writes, “No single factor can explain why food is so much more expensive now than before the pandemic. Food prices—which are up 34.6% since 2019—remain high because of the combined impact of rising input costs, supply chain disruptions, and corporate profits.”

Little Decisions Can Lead to Big Relief

Sports

I have a friend who is the father of six children. He and his wife made a decision to simplify their lives and ease the cost of youth sports. Their rule was that if the child wanted to be in sports, the only sport they could do was running because it was the least expensive, it was good for them, and they could practice it anywhere. All of them turned out to be capable runners. Consider a similar narrowing of sports options to protect your time and expense. Furthermore, ride sharing with other moms can help ease your costs and nerves.

Health Care

Look into health care co-ops. Many people are moving to this lower-cost alternative to health insurance. Practice preventive medicine by monitoring your children’s diet with healthy options instead of fast food.

Groceries

It is wise to purchase in bulk to capture available discounts. Check into:

Housing

While I understand you may be cramped in a smaller home, find joy and contentment where you are now. Stress increases when we live in the future. We know young couples who rent to enjoy low maintenance and flexibility, while others are looking at smaller homes to avoid the high costs associated with a bigger one.

Steps to Avoid Being Overwhelmed

Be optimistic and grateful. Invite the children and like-minded friends to participate so you can encourage one another. Limit time with those who are big spenders. Here are some other ideas:

Got Debt?

Credit card bills that are not paid off monthly are harming the financial state of many American families. Aim to pay off the one costing you the most in interest first. Apply any extra income (raises, tax refunds, gifts, etc.), savings from cooking at home, and reduced expenses (like a low utility bill) to that debt. When that one is paid off, direct the money toward other interest-bearing debt, and put some toward building your emergency fund.

Set specific goals, and eventually build short- and long-term savings. Plan ahead for future needs: car and home repairs and maintenance, school supplies and uniforms, etc.

Study your bills to gain insight into how to reduce them. For example, what grocery or household purchases are more inflated than others? Try doing without, finding substitutions, or making your own, like salad dressing, bread, and cleaning supplies. Research options online.

Use “Taxi” Time Wisely

Keep It in Perspective

In November 2008, Zimbabwe experienced the second-highest recorded inflation rate in history. It reached a peak of 89.7 sextillion (10²¹) percent.

Not long ago, I was attending an economic forum where a panel of Americans discussed their concerns over “double-digit” inflation, as if it were unbearable. During the exchange, a few Zimbabweans offered consultation by explaining how they survived the second-worst hyperinflation ever recorded. They watched their money become worthless; yet they found joy in the midst of a financial meltdown. God brought them through the crisis, and many look back on their losses as a blessing in disguise, as their priorities dramatically shifted toward appreciating all the things that money cannot buy.

Consider posting a card or note in a prominent place in your home that expresses your gratitude for all the small things that bring you joy each day. Counting your blessings will have a positive impact on you and your family.

Additional Resources

Crown has many biblically based, practical, and empowering courses and studies that can help you find freedom with your finances. Learn how to be a faithful financial steward of the resources God provides.

This article was originally published in The Christian Post on April 10, 2026.

Dear Chuck,

Is there such a thing as depression brought on by financial stress? We have reached midlife and have very little to show for it. It seems we had money but not enough common sense to set some aside for our retirement years, which are quickly approaching.

Depressed About Our Finances

Dear Depressed About Our Finances,

I am sorry that you are experiencing depression; your comments remind me of what Christ taught us: “Life does not consist in the abundance of possessions” (Luke 12:15 NIV). Your finances should not determine your worth, happiness, or meaning and purpose in life.

Have you ever made a list of the things that have brought joy to your life that money cannot buy? It is a great exercise to fight off the grip of depression. The list could include friendships, shared experiences, love, children, church, and the things you have done to serve God and others. This will help you see the truth that your true riches in life do not come from money and possessions.

Change Is Possible

It is true that the use of money and resources early in life strongly impacts one’s future. The reality of past spending and lack of preparation can cause deep guilt and fear.

According to an article at Mental Health Hotline, the toll of financial stress has been linked to the following:

Thankfully, those actions or past mistakes do not have to be final. The financial, emotional, and relational challenges are real, but it is never too late to change course. In fact, midlife can be the most powerful season for transformation because your motivation is stronger, your awareness is higher, and your understanding of what habits need to change is clear. Comparing your life to others may only add to the financial stress. The strain can lead to hopelessness if relief is not in sight.

“Therefore do not be anxious about tomorrow, for tomorrow will be anxious for itself.

Sufficient for the day is its own trouble.”

(Matthew 6:34 ESV)

Take Agency—Plan for a Better FutureSome simple steps can set you on a path to find hope:

Money Doesn’t Last—Eternal Riches Do

What we accumulate on earth can be lost, stolen, or devalued. It will ultimately all be left behind. No matter how big or how small your net worth is, you won’t be taking it with you. We come into the world naked and leave the same way. Remember, a naked person has no pockets.

Earthly wealth will provide temporary comfort and hope for provision later in life. But eternal riches will grant you lasting peace and reward. Choose to live with an eternal perspective. You will find that stewarding what God gives you has a whole new meaning and purpose.

Take this time in your lives to surrender everything to Him. Then ask Him to give you the wisdom, discipline, and desire to live as His financial manager. He is faithful, merciful, and abounding in steadfast love and kindness. Refuse to listen to the attacks of your accuser—even if you have setbacks. Stay the course, and remain faithful to Him.

One day, you can look forward to hearing, “Well done, good and faithful servant. You have been faithful over a little; I will set you over much. Enter into the joy of your master” (Matthew 25:21 ESV).

“Do not lay up for yourselves treasures on earth, where moth and rust destroy and where thieves break in and steal, but lay up for yourselves treasures in heaven, where neither moth nor rust destroys and where thieves do not break in and steal. For where your treasure is, there your heart will be also.

(Matthew 6:19–21 ESV)

Financial stress isn’t just a numbers issue; it’s a trust issue. Inviting God into our decisions replaces fear, guilt, and anxiety with His peace that passes all understanding.

Additional Resources

If credit card debt is adding to your stress, consider reaching out to Christian Credit Counselors. They are a trusted partner of Crown and are able to help consolidate debt and get one on the road to financial freedom.

This article was originally published on The Christian Post on April 3, 2026.

Dear Chuck,

We are juggling careers and family and cannot find the time to cook at home. We are spending a ton of money eating out or ordering meals to go. It is getting ridiculously expensive. My husband and I know we have a problem, but we can’t seem to change our habits.

Eating Out Too Much

Dear Eating Out Too Much,

Your future is determined by the financial decisions you make each and every day, whether small or large. One that far too many people are making revolves around eating out or ordering in. Grocery and meal delivery became popular during the COVID-19 pandemic, and the convenience has been hard to overcome.

An article at NerdWallet addresses the trend. It cites a statistic from the National Restaurant Association: “In 2024, nearly three out of every four restaurant orders were taken to go.”

Many claim exhaustion in trying to balance work and family.

For some, the cost is not a problem. For others, the cost can be unmanageable. Just $20 (the cost of a sandwich plus tip and fees) a couple times a week comes out to $160/month. For a family of four, that’s $80 twice a week or $640/month or $7,680/year. That is a lot of money that could go toward many other family priorities, like an emergency fund, debt repayment, a retirement account, a house, a vehicle, Kingdom building, etc.

Is Eating Out Worth It?

Stephanie Gravalese reports that rising menu prices, growing delivery surcharges, and concerns over portions and quality are leading consumers to rethink eating out:

Change Your Mind; Your Habits Will Follow

Food is a gift from God that He provided at the creation of the world. Meals prepared at home bring comfort, build memories and relationships, and provide opportunities to practice hospitality and share our hearts with each other. It is a form of communion when we break bread with others.

If you “cannot find the time to cook,” I suggest you take a serious look at your life:

I don’t know your situation, but it may be time to have an important conversation to see if this is how you truly want to live. The Apostle Paul wrote about orderly worship, saying, “But all things should be done decently and in order” (1 Corinthians 14:40 ESV). If we apply that to home, work, and life in general, we experience peace and predictability in our days.

My wife, Ann, who does a great job working from home and also preparing our meals, found a notable article that goes deeper into a plan to break the eating-out habit. Others are also listed below.

Is a One-Income Family Possible? How about Working from Home?

Our late founder, Larry Burkett, author of Women Leaving the Workplace, said that the financial benefits of staying home will generally offset the loss of income. His extensive research showed that the decision lowered costs of childcare, transportation, and work attire. He died before the phenomenon of take-out and meal delivery, but if he were still alive, he would be shocked at the money spent on it.

He suggested that families learn to budget effectively and prioritize their financial goals in order to live on a single income. Seeking remote work, a hybrid model, or a home-based business can provide the flexibility needed to manage finances and make cost-effective decisions. It does not have to be permanent. The idea may seem daunting and completely contrary to what the world deems necessary, but the results pay dividends.

Fox News featured Mary Neilis, a Westchester, New York, mother of seven, earlier this year. She turned her nightly family dinners into a full-time job after her “7kidskitchen” went viral on TikTok. On Fridays, she does meal planning and online grocery ordering, taking advantage of sale items in her menus. Mary explains, “If chicken’s on sale, we might have three chicken dinners that week. If steak is on sale, we might have steak fajitas that week.”

The Key: Get Organized

Once you develop a routine, shopping, cooking, and eating at home become easier. Get to know your family’s likes and needs, and learn some basic recipes. Keep it easy, recognizing that meals don’t have to be gourmet, although you can make them feel that way by using candles, flowers, etc.

Some families have the same breakfast every day and consistent meals, like Taco Tuesday and homemade pizza on Fridays. I suggest you develop your own strategy to keep things simple. Try cooking as a couple or rotating meal duty, and give children age-appropriate kitchen chores. The lessons learned about budgeting and eating at home will help them tremendously.

Benefits of Cooking at Home

Challenges to Try

Proverbs 31 says that a woman who fears the Lord is to be praised. An excellent wife plans ahead, and her household is blessed by her efforts. The key is making it a priority for both husband and wife. Ann does most of our shopping and cooking. I never learned to cook, so I am not much help, but I’m happy to pick up things she needs and always do the dishes. We unload the dishwasher together and do other kitchen duties as a team. “She rises while it is yet night and provides food for her household…” (Proverbs 31:15 ESV). My wife adds, “And the husband who helps is greatly appreciated!”

Extra Reading:

3 Little Things That Are Wrecking Your Budget

A Tip for Saving Money on Food

Whether you’ve been part of Crown for years or are just discovering us, we’d love for you to be part of our 50th Anniversary Celebration. For five decades, Crown has taught biblical stewardship principles that transform finances, strengthen families, and deepen faith. Lives have been changed. Communities have been empowered. Purpose has been rediscovered. And we’re just getting started!

This article was originally published on The Christian Post on March 27, 2026.

Dear Chuck,

My husband and I are 28. We would love to start a family, but I don’t know how we can afford it, even with both of us working. Do you have a financial plan for starting a family?

Yearning for Children

Dear Yearning for Children,

Thank you for your question and desire to begin a family. In short, yes, you and your husband can and should make plans to start a family!

We are in a trend of what I call “delayed marriages/delayed families.” The formation of a traditional nuclear family is at an all-time low in American history. I read a few years ago that the American family of the future will likely be “1.8 children and 2 pets.” I hope you will help reverse that trend. Let’s address the common reasons why fewer young people are having large families.

Population Fears

Just this week, Dr. Paul R. Ehrlich, author of the book The Population Bomb, passed away at age 93. His bestselling book of the ‘70s was filled with doom-and-gloom predictions of mass starvation due to overpopulation. I found his work nothing more than disgusting, unsubstantiated fear-mongering. The world is not overpopulated—not even close. That is a lie against God and a distortion of the scientific facts. One tongue-in-cheek but appropriate comment to his obituary read:

“Dr. Paul R. Ehrlich is survived by 8,300,678,394 people (134% increase from 1968), with a daily worldwide average calorie intake of 2,800 kcal (a 22% increase).”

Financial Fears

Born on an Indian reservation, my grandmother’s crib was a vacant dresser drawer. They had very little money, but God provided. My wife’s parents had five children in a two-bedroom, one-bath house. This was normal in our generation. But not today.

Many fear the expense of raising children. The truth is, Satan hates families and will do everything in his power to prevent or destroy them. Today’s “needs” were yesterday’s luxuries that many cannot imagine doing without. Yet they come with a cost that is shrinking families and decreasing fertility.

Thankfully, there are still couples who are committed to raising children to impact the world for Christ. Two of my nieces have five and six children each. They are stay-at-home moms who refuse to get caught up in the materialism of today’s society. They have chosen a simple, wholesome lifestyle with Christ at the center and are raising a happy crew of kiddos.

Biblical Perspective

In Luke 2:24, we read that Mary and Joseph brought Jesus to the temple to honor the Jewish law for newborn boys. They could not afford a lamb to sacrifice, but “a pair of turtledoves or two young pigeons” was an acceptable offering to fulfill the law. They recognized their financial position and humbly obeyed God’s Word. So should we.

Make a Plan

Accept where you are without comparing yourself to others. Understanding who you are in Christ will give you the confidence to live “contra mundum.” The world will tell you everything you “need” to outfit a nursery, how to dress fashionably during pregnancy, where to take a “babymoon,” the best childcare available, and so on—basically telling you how to spend your money (or max out your credit cards). Many projected costs are higher than necessary for those who are consciously dedicated to living on a conservative budget.

Financial preparation is important to prevent stress during and after pregnancy. It is achievable by sacrificing for the greater good of a family. Choosing to live modestly does not mean you have to suffer. It simply means setting boundaries and prioritizing spending. Refuse to get too comfortable in this world by focusing on eternity, not on earthly desires. Be creative in finding ways to enjoy living free of financial worry and “keeping up with the Joneses.” The “Joneses” are probably in debt anyway.

Things to consider:

Begin living on one income while using the other to build emergency savings. Pay down high-interest debt, like credit card balances. Create a budget that will enable you to save while simultaneously paying off debt. Be willing to adjust your lifestyle dramatically. This will create margin, especially if housing and vehicle expenses can be reduced. Bump up contributions to your Health Savings Account (HSA) so tax-free dollars can be used for medical expenses. Don’t forget to give first.

Start buying groceries regularly and cooking at home. Learn to make freezer meals. These will help once a baby actually arrives. Family, friends, and YouTube can provide recipes and cooking lessons.

Look for free entertainment without the cost of subscriptions and streaming, which add up over time.

Resist the temptation to hire professional photographers, have elaborate celebrations, or decorate a magazine-worthy nursery. Learn to be content with simplicity and a life free of financial stress. Find like-minded friends with whom you can do life.

Sell what you don’t need. Limit time on social media to avoid impulse spending or the desire for perceived needs. Save, get good health insurance, and write a will.

If you believe people will offer to have a baby shower for you, begin making a list of true essentials. Don’t spend any money until absolutely necessary. Instead, ask God to provide. If and when things are needed, you can borrow from family or friends or shop Facebook Marketplace and thrift stores. Don’t rob yourself of the joy of having your prayers answered by impatiently getting ahead of God.

Reject the nonsense found in The Population Bomb, and renew your mind on God’s truth:

Behold, children are a heritage from the Lord, the fruit of the womb a reward.

Like arrows in the hand of a warrior are the children of one’s youth.

Blessed is the man who fills his quiver with them!

He shall not be put to shame when he speaks with his enemies in the gate.

Psalm 127:3–5 ESV

Further Reading

Children Are a Blessing… And an Investment

Crown has many biblically based, practical, and empowering courses and studies that can help you find freedom in your finances and career. Learn how to be a faithful financial steward of the resources God provides.

This article was originally published on The Christian Post on March 20, 2026.