Dear Chuck,

We have a budget, but the cost of groceries and eating out is ridiculous! Something has to change. What can we do? We are exceeding our food budget every single week.

Fed Up with Grocery Prices

Dear Fed Up with Grocery Prices,

You are correct. Something does have to change for almost all of us who are being pinched by the price of food. I am fortunate that my wife, Ann, who does research on all of my articles, is also a great grocery shopper, so I asked her to contribute her insights, which greatly helped my reply.

Has Greed Taken Over the Food Industry?

Hmm, supply-chain issues have been resolved, cost pressure from the war in Ukraine has eased, stores are stocked with inventory, compulsive pandemic shopping has ended, and employees gained higher wages, so why are grocery prices still inflated? Have you heard of “greedflation”?

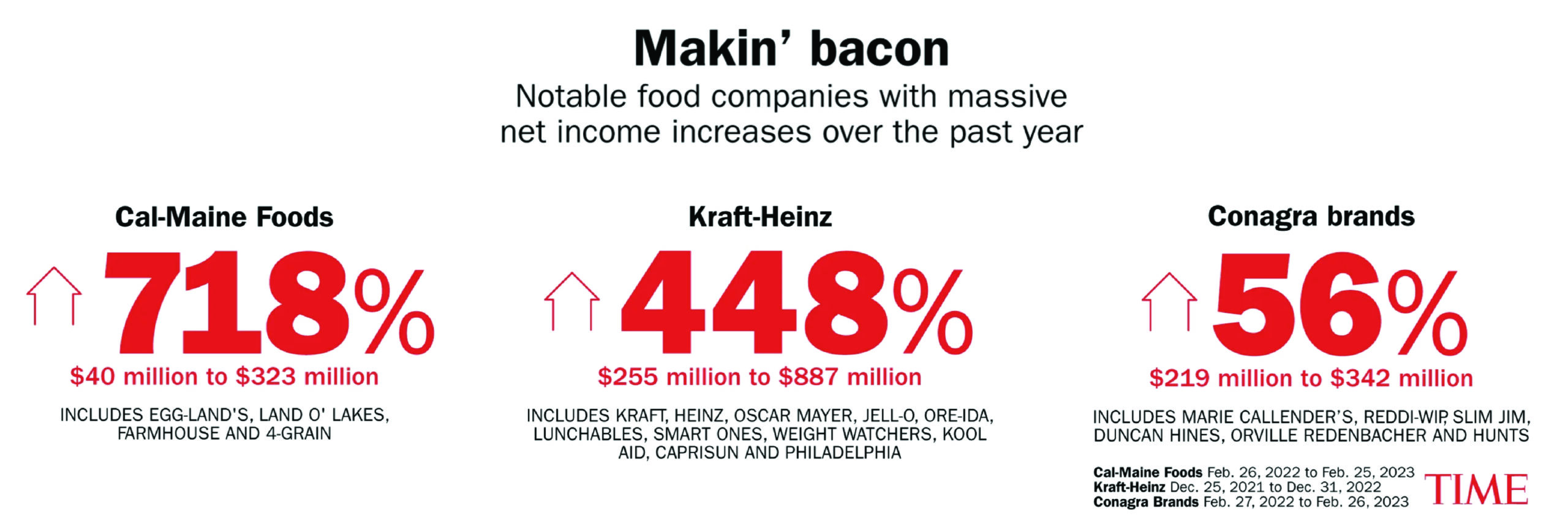

Eggs are 70% more expensive than they were a year ago, with many stores limiting purchases to two dozen. Other staples remain elevated in price, while only a few things have come down. Several explanations are possible. Mergers in the food industry have resulted in few competitors. Profit hoarding, or as some call it, “greedflation,” occurred when corporations amplified disruptions to their benefit. See the staggering numbers here or in the graphic from Time Magazine below.

Businesses know that people will pay more for what they want, so getting them to forfeit profits will be tough. The ultimate solution will come when leaders are willing to sacrifice millions (billions) of dollars in bonuses, perks, and salaries for the good of the nation. Inflation tends to be “sticky” or hard to get rid of. Don’t count on it going away soon; so in the meantime, you must get proactive.

Ideas from Ann, My Money-Saving-Grocery-Shopper Extraordinaire

One obvious way to reduce your bill is to go on a diet. Seriously!

Reduce your consumption of sugar, meat, soda, juices, alcohol, and prepackaged foods/snacks. Compare unit prices using a calculator if necessary. A shopping list app or shopping guide may be helpful. In addition, avoid eating out for a month, and see how much you save. Here are some other helpful hints:

Wonder what you should be spending? The USDA compiled a Thrifty Food Plan Cost guide.

The internet offers many budget-saving recipes. Bon Appetit even has a list of cheap dinner ideas.

Become an expert at saving money on groceries. Meet regularly with friends to share cost-saving tips and recipes. Notify one another of sales, and share items you find. Learn to make all that you can from scratch, from salad dressings to snacks. Involve the whole family, and praise each other’s attempts to fight this battle.

Try not to complain, especially in front of your spouse or children. Remember the Israelites whom God rescued out of Egypt? He provided for their every need, yet they failed to meditate on His goodness. They did not give thanks. Instead, they wept in self-pity and said, “Oh that we had meat to eat! We remember the fish we ate in Egypt that cost nothing, the cucumbers, the melons, the leeks, the onions, and the garlic. But now our strength is dried up, and there is nothing at all but this manna to look at.” (Numbers 11:4–6 ESV)

Being mindful of this, focus on what you do have. Ask God for help. Then give thanks, and celebrate discounted items or delicious cost-saving recipes you find. Enjoy potlucks with friends or neighbors. Enjoy a “Cheapest Meal Competition”—that must also be delicious! Try memorizing Psalm 100, and give thanks at every meal. Pray for those who literally have no food or can only afford one meal a day.

Thank you, Ann.

Economic Cycles

It has been said that the best cure for high prices is high prices. People tend to pull back spending when it no longer makes sense; thus, demand drops until prices also decline. By becoming more frugal during this time, your spending habits will help accelerate a price adjustment in the long run. Thank you for the question.

The Crown God Is Faithful devotional can offer some inspiring and practical Biblical wisdom in such uncertain times. You can subscribe to receive daily devotionals that will help transform your finances and provide much-needed encouragement. May it be a blessing!

This article was originally published on The Christian Post on May 5, 2023.

Dear Chuck,

I would like to eliminate our high interest credit card debt. What are your thoughts on taking out a HELOC to pay it off?

HELOC or NOT?

Dear HELOC or NOT?

Just to be sure readers know what we are talking about, HELOC stands for Home Equity Line of Credit. It is a line of credit that uses the equity in your home as collateral. Because of high interest rates and inflation, more and more homeowners are using a HELOC. The rates are usually more favorable than other forms of consumer debt, especially credit cards. This revolving line of credit is quickly replacing the older method of “cash out refinancing.” It can be helpful when used wisely because it gives homeowners access to equity to help meet cash flow needs—emphasis on the word wisely.

General Thoughts on HELOCs

Paying off credit card debt can be a good use of a HELOC for the disciplined spender. You must strive to reduce the use of credit cards and faithfully pay off the balance every month to avoid accumulating high cost debt again. Know, too, that if repayments of the loan are missed, you face the danger of foreclosure. So your decision must first be based upon your personal discipline to keep within a budget and a plan.

A home equity loan pays a lump sum at a set interest rate, whereas a HELOC allows funds to be taken as needed. This keeps monthly payments lower and helps avoid unnecessary debt. Some nominal costs are involved, and interest is only charged on what is borrowed. However, the rate is typically variable, and the payout period ranges from 10 to 20 years.

To qualify, verifiable income, good credit, and considerable equity are needed. Reliable payment history may be investigated. See Bankrate.com or Forbes for current HELOC rates. Lenders will use Loan-to-Value (LTV), Combined Loan-to-Value (CLTV), and Debt-to-Income (DTI) ratios as well as other factors to determine individual interest rates and the amount eligible to borrow.

Terms to Know

Pros

Cons

When to Use

When to Avoid

HELOC or NOT?

The best use of a HELOC is to increase property value. The risk is that one’s home is used as collateral. If convinced this kind of borrowing will be beneficial, compare rates and fees of different lenders. Understand the repayment structure and all requirements before signing any paperwork. What is the prepayment fee and policy? Does a low monthly rate come with a balloon payment? Will a shorter repayment timeline grant a lower rate? Is there an inactivity fee? Does your bank or credit union offer member discounts?

Once the loan begins to amortize, monthly payments can be painful unless the borrower is disciplined and prepared. That is why I recommend that a payback plan be in place before borrowing any money.

“The rich rules over the poor, and the borrower is the slave of the lender.” (Proverbs 22:7 ESV)

The Bible warns of debt becoming a form of slavery. Avoid presuming on the future—especially during uncertain economic times. And do not borrow to simply keep up with friends or neighbors. While a HELOC can be helpful in extreme cases, I always think it is best to make a plan to pay off the debt causing you pain without creating more debt. For most people, this is a safer and wiser path to financial freedom.

My bottom line: paying off high debt with a low rate HELOC can be wise if the Lord directs you in this way. Pray for wisdom.

Christian Credit Counselors is a trusted source of support in assisting people with getting on the road to financial freedom. Reach out to them today; they may be of great benefit to you.

This article was originally published on The Christian Post on April 28, 2023.

Dear Chuck,

My husband and I believe America has lost its way. I see so much pride, division, financial fear, and greed that I wonder if we can even recover. How can an individual make a difference?

Overwhelmed by America’s Decay

Dear Overwhelmed,

You, like so many others, are expressing a sense of gloom that has come over the nation. As believers, we are inwardly groaning at what we see happening to the nation that once stood as a beacon of light to a dark world. And your concerns are reflected in the data.

According to findings in a recent survey by the Wall Street Journal, traditional or core American values are declining, while the value placed on money is increasing:

The loss of values that unite and the increase in the value placed on money are dangerous trends. Most tension, family friction, strife, anger, and frustration are caused directly or indirectly by money. Christians have access to Biblical financial principles, but do we implement them? Many do not—either by choice or ignorance.

Love Is Not Proud

C.S. Lewis called pride “the great sin.” He said, “Pride is spiritual cancer: it eats up the very possibility of love, or contentment, or even common sense.”

If we humble ourselves before the Lord, individuals can make a difference, and God has given us clear instructions on what we are to do!

God is love and desires that we use what He provides, whether great or small, to love Him and others. Jesus said, “You shall love the Lord your God with all your heart and with all your soul and with all your strength and with all your mind, and your neighbor as yourself.” (Luke 10:27 ESV) This applies to every area of our lives—even finances. Do you know anyone who models this well? If not, can I challenge you to become that person? The world needs examples!

Below are three ways you can begin to make a difference.

Financially Love Your Family

No matter how much our culture drifts away from God, we are to care for the needs of our families. This includes their financial, spiritual, and emotional needs:

Financially Love Your Church

We can plug into our local, Bible-believing, gospel-centered church and support its mission and programs. Change happens in community, and the church was created to strengthen one another as we serve others in love:

Financially Love Your Neighbors

We are to care for one another in word, deed, and dollars:

America Is Not Our Home

The core problem is that the world has been ravaged by sin since Adam and Eve disobeyed God’s commands. We need personal redemption from the sin that has controlled us and a kind and generous heart toward those who remained trapped in the darkness.

While we are blessed to live in America, I am constantly reminded that it is only our temporal home. Let’s do all we can to be salt and light until our journey here is complete.

The Crown God Is Faithful devotional can offer some inspiring and practical Biblical wisdom in such uncertain times. You can subscribe to receive daily devotionals that will not only help transform your finances but will also provide much-needed encouragement. May it be a blessing!

This article was originally published on The Christian Post on April 21, 2023.

Dear Chuck,

Our finances are stretched so thin that I am stressed out all the time. We live on a budget, but my husband and I both need some hope that it will not always be this way.

Living on a Financial Cliff

Dear Living on a Financial Cliff,

There is certainly reason for hope, so hang on!

Let’s put your challenges in a current economic context and then a Biblical context before I offer some practical tips to help you through this painful time.

Economic Context

With the lingering impact of inflation, a new CNBC survey reports that 70% of Americans say they, too, are feeling financial stress, and 58% report they are living paycheck to paycheck. The report pointed to several specific concerns, including a lack of savings and a dependency on debt.

“People are worried that the money they’ve saved won’t last and are worried they’re going to have to lean more on their credit cards and other sources of debt just to get by,” said Bruce McClary, a senior vice president at the National Foundation for Credit Counseling.

With rapidly increasing costs, higher interest rates, and a sense of economic uncertainty in the air, many are feeling like their finances are balanced on a razor’s edge with no margin for error.

Biblical Context

The Bible is full of people who had to face incredible amounts of stress. It is also full of principles and truth that help us to reframe our present circumstances. I am reminded of Romans 8:18–21:

I consider that our present sufferings are not worth comparing with the glory that will be revealed in us. For the creation waits in eager expectation for the children of God to be revealed. For the creation was subjected to frustration, not by its own choice, but by the will of

the one who subjected it, in hope that the creation itself will be liberated from its bondage to decay and brought into the freedom and glory of the children of God. (NIV)

We live in a fallen world—in bondage to decay—because of mankind’s disobedience to God, but a promise of freedom and redemption awaits those who are children of God. Considering our eternal future, our present trials and tribulations are insignificant. Remember to keep your present cares and burdens in the context that this is not our home. We temporarily manage what God provides and seek to be faithful until we have finished our race.

Help in Reducing Your Financial Challenges

Three very practical steps will help you reduce the immediate pain you are in.

First, no matter how much or how little income you have each week or month, be sure that you are spending less than that amount. Think of the old game of limbo, where you have to bend your body to get under a bar without knocking it off. The bar represents your income. Your attempts to get under it represent your control over your spending. That is why a budget is so very helpful. You can adjust your expenses to ensure that you never exceed the height of the bar (your weekly or monthly income).

Second, build an emergency savings fund. You need at least $1,000 set aside to help with unexpected expenses. That is the bare minimum. Set a goal of saving three months of overhead. Emergencies always happen, so this is non-negotiable. In the CNBC survey, most of those who report living paycheck to paycheck say they do not have any money saved. This is like flying through the air on a trapeze bar without a safety net. It is scary! Crown has some free tools to help you get that accomplished. Perhaps you need to adjust your budget. You might benefit from our budgeting resources and a coach.

Finally, make a plan to reduce your debt and break any dependence on credit cards, store accounts, buy-now-pay-later plans, or payday loans. The largest expense in most American budgets today is interest expense on debt. Just imagine how free you would feel without debt hanging over you each month. We partner with Christian Credit Counselors to help free people from this burden.

Thank you for writing. Please know that we want to help! May God give you His peace and the freedom you so desire.

Christian Credit Counselors is a trusted source of support in assisting people with getting on the road to financial freedom. Reach out to them today; they may be of great benefit to you.

This article was originally published on The Christian Post on April 14, 2023.

Dear Chuck,

It sure looks like Larry Burkett’s book “The Coming Economic Earthquake” is happening before our very eyes! Is this the big one that he warned us about?

Economic Observer

Dear Economic Observer,

It would be hard to overestimate the number of times I have been asked this question in the past 22 years that I have worked with Crown. So my answer is always the same, “No, not yet.” Let’s review a few key points from Larry’s book that you referenced, and then I will add my thoughts about the times we are in now.

The Coming Economic Earthquake

Larry authored his best-selling book in 1991. Within the pages, Larry discussed economic history, the US government’s violations of Biblical principles of sound money, and the plausible scenario for what could happen to the debt-fueled American economy. He was careful to say that he was not a prophet, nor could he tell the future, but he was compelled to warn about the possibility that America’s economy could be destroyed within ten years of the publication of his book. That was 32 years ago.

Fortunately, the American economy has survived a number of very significant challenges since then, including the Great Financial Crisis of 2007–2008. Larry’s timing was way off. He was labeled an alarmist, and many discredited his thesis altogether. But let’s take a look at the argument that Larry made and compare it to where we are now, three decades later.

At that time, an estimated 20% of the annual budget deficit was funded by foreign investors. That number has increased to 30% in the estimated federal budget proposed for the coming fiscal year.

An article on Schiffgold says: “Since March 2020, the federal government has added $4.7 trillion to the national debt. And as WolfStreet put it, the Federal Reserve went ‘hog-wild’ with debt monetization. . . . At some point, the central bankers will be faced with a choice – continue monetizing the debt and inflating the money supply or deal with surging inflation by letting rates rise. It can’t do both. And neither of these choices will play out well for the American people.”

As Larry Burkett said, “What is the national debt but the visible indicator of gross fiscal mismanagement on the part of our leaders?”

Where Are We Now?

All of the warning signs that Larry wrote about are certainly still in play. In fact, they have been every year since he first penned the book; however, the American economy has shown incredible resilience to shocks and has expanded more than Larry may have ever dreamed or imagined. Through economic expansion and federal monetary policy, “the big one” has been staved off far longer than Larry and many other experts thought would be possible.

In Deuteronomy 28, God gave clear economic instructions to His chosen people: “And if you faithfully obey the Lord your God, being careful to do all his commandments that I command you today, the Lord your God will set you high above all the nations of the earth.” The promises for obedience that follow are for blessings of abundance and strength, including verse 12b: “…And you shall lend to many nations, but you shall not borrow.” However, the curses for disobedience would undo all their progress, including verses 43–44: “The sojourner who is among you shall rise higher and higher above you, and you shall come down lower and lower. He shall lend to you, and you shall not lend to him. He shall be the head and you shall be the tail.”

America was the largest creditor nation in the world in the late-‘70s but flipped to the largest debtor nation in the world by the mid-’80s. Our nation is facing an ever-increasing mountain of debt and a potential banking crisis while attempting to control inflation and fight off a recession or worse. I cannot help but believe it is all related to our declining interest in obeying God. The heart of our economic problem is truly the heart problem of our people. Until we believe God is needed here, we should not expect to avoid an economic crisis.

An economic earthquake will come; we just don’t know when.

In such uncertain times, the Crown God Is Faithful devotional can offer some inspiring and practical Biblical wisdom. You can subscribe to receive daily devotionals that will help transform your finances and provide much-needed encouragement. May it be a blessing!

This article was originally published on The Christian Post on April 7, 2023.

Dear Chuck,

This banking crisis has me nervous. How bad is it? Should we trust our small regional banks? Where should we put our money?

Widowed and Worried

Dear Widowed and Worried,

As you are, we should all be concerned and paying attention. This is a very real and dangerous economic challenge.

What Happened?

Silicon Valley Bank and Signature Bank are the 2nd and 3rd largest bank failures in U.S. history, topped only by Washington Mutual, which collapsed in the financial crisis of 2008. 94% of Silicon Valley’s deposits were uninsured, as were 90% at Signature. SVB had a concentration of tech startups, and Signature had a significant number of holders of cryptocurrencies. Together, the banks held combined assets of nearly $320 billion.

The assets at SVB were too heavy in long-term treasury bonds that were purchased before the Fed raised interest rates. Their value decreased as investors preferred new bonds that earn higher rates. Rather than analyzing the market value of the bonds, the accounting value gave a false portrayal of the bank’s status. To calm a run on banks, the current administration guaranteed uninsured deposits at both banks, and the Federal Reserve announced a lending program for institutions needing to borrow money to cover withdrawals. Over time, the FDIC fund will have to be replenished, possibly by a “special assessment” on banks that customers will undoubtedly have to pay in fees.

“The principle of sound money was ignored by the Fed. SVB violated principles of diversification and prudence. It set aside its fiduciary duty to steward the assets of others and focus on business, not ideology.” (Jerry Bowyer)

Bank Contagion

I don’t pretend to be an economist or understand the complexity of the current banking crisis. I do know that the First Republic Bank is also distressed and had to be rescued by its rivals. Credit Suisse, a century-old European stalwart bank, had to be rescued by rival UBS (United Bank of Switzerland) for it to remain solvent. While some are calling for more bank reform and regulation as the solution, the Federal Reserve is working overtime to stop runs on banks and ease the fears of depositors like you and me. By some indications, as of this writing, those measures are working to diminish the fear of a complete banking meltdown.

What To Do with My Money Now?

An in-depth article in Fortune Magazine gives insight into the history of bank failures and some helpful advice on managing your bank accounts. Here are a few tips from my perspective:

The Economic Finger Trap

One side of our economic challenges can be solved by controlling inflation, which requires raising interest rates. The other side can be controlled by increasing liquidity in our banks, thereby increasing inflation. Some say the Fed will be choosing between generational inflation and another banking crisis in the days ahead.

“A prudent person foresees danger and takes precautions. The simpleton goes blindly on and suffers the consequences.”

Proverbs 27:12

The coming days will be interesting indeed. This should be a wake-up call to millions of people, especially Christians. We need to live prepared for any of these possible scenarios.

The Crown God Is Faithful devotional offers inspiring and practical Biblical wisdom. You can subscribe to receive daily devotionals that will help transform your finances and provide much-needed encouragement. May it be a blessing!

This article was originally published on The Christian Post on March 24, 2023.

Dear Chuck,

My husband and I bought our first home in an older neighborhood where young families are choosing to live. We put 10% down and now want to build equity in our home, but we have more time than money. What are the best ways to build “sweat equity” as “do-it-yourselfers”?

First-Time Homeowners

Dear First-Time Homeowners,

Congratulations! I am happy for you and want to give some solid advice to a question that is more complicated than it may seem.

Get Rid of the PMI First

Because you qualified for a mortgage without having the desired 20% down payment, you are now required to have Private Mortgage Insurance (PMI). Getting rid of this should be your first and highest priority, as it adds costs and impedes your progress in actually owning your home. Nerd Wallet offers great advice and options for your consideration. Regardless of the method you choose, get out of it before you start any projects on building equity.

Building Equity

Many people have moved over the past few years, and some hope to become homeowners this year. The value of your home and the ability to build equity can fluctuate wildly by region and economic conditions, so let’s discuss the topic of equity.

Equity is the amount of the home that actually belongs to you. If your home is worth $400,000 and you owe $150,000, then your equity is $250,000 (market value – loan balance = equity). Your equity grows as the value increases and debt decreases. Why is equity important?

Not All Real Estate Is a Good Investment

It is true that historically the best pathway to building personal assets in America has been homeownership. But that is a very broad assumption. I have counseled many young couples who have lost their shirts by buying a home, especially when sinking money into a project that they may never recover. In fact, this happened to me when Ann and I were first starting out as a couple. Let’s help you avoid that by being very careful with the decisions you make to create “sweat equity.”

Improve Value and Build Equity

Any improvements or upgrades should fit the neighborhood to ensure you get the value back at resale. Do not overspend. You are much better off having the least expensive home in a nice neighborhood than the most expensive home in a so-so neighborhood!

Upgrades vary depending on the location and home values in your neighborhood. Know what upgrades will truly benefit the home. Check with realtors or appraisers. Don’t ignore problems. Maintain instead of waiting to repair. This is a basic financial principle of home ownership. Even though you want new countertops, a leaky roof must be repaired or replaced because it protects the entire house for decades to come. Adding some paint will likely be a much better investment than a swimming pool. Know your market before deciding where you will spend money and time on improvements.

Any work you do yourself can greatly increase your equity. Make a plan, set goals, and then set aside time and money for the projects. Take your time, and shop sales. YouTube is a great source of valuable instruction. Recruit friends to help you, and be willing to return the favor. It makes the work more rewarding and builds a tight community. I have practiced this with neighbors wherever we have lived.

Sometimes value is gained by adding square footage via an attic or basement. This is often less costly than actually adding on to the house. Again, it depends on location. A garage apartment or guest house may increase a home’s value and be an added source of income.

Impact on Neighborhood

People will notice the care you put into your property. Your work may encourage neighbors to do likewise. This can improve the value of your entire neighborhood.

Homeownership requires adequate emergency savings. An older home may have really strong bones, but maintenance and repairs are a fact of life. Stay on top of these. Do not procrastinate when a sign of a problem appears. Stay ahead of any issues!

Here are a few good resources:

Caring for your home means you are always in a position to sell should the need or desire occur.

Keep an eye on the market, and do not overdo it. Continue to replenish your emergency funds. Care for your home as if it were the Lord’s. Make it a place to welcome others and a place of rest for your soul. If done right, your time and money will likely increase market value and equity over time.

Another important way to make strides in your financial health is to diligently pay off credit card debt. Christian Credit Counselors is a trusted source of support. They specialize in assisting people with getting on the road to financial freedom.

This article was originally published on The Christian Post on March 17, 2023.

Dear Chuck,

We like our bank, but we get next to nothing while they hold our money in checking and savings accounts. We need to do better, but we fear moving money to banks we do not really trust. What would you do?

Looking for a Better Return

Dear Looking for a Better Return,

A December 2021 Bankrate survey found that, on average, customers kept the same savings account for almost 17 years and checking accounts for nearly 18. The main reason is no or low monthly fees. Other reasons are that they have always had the account, they are happy with the customer service, there are convenient branches/ATMs, and it is too much of a hassle to change. This matched our personal profile exactly!

My wife and I recently decided to move some of our savings into short-term CDs to get a better rate. We expressed a desire to our bank that they match competitors’ CD rates. It has been a week since we spoke with our bank, and we are still waiting to hear back. In the meantime, we continue to conduct research.

We also asked if we could earn a better rate on the funds we keep in our savings account. Surprisingly, we were told that since we opened that account at an older branch, if we moved it to the “new” location, closer to our home, we could earn a much higher rate. I wondered, “Why in the world weren’t we told that months/years ago?” Then it dawned on me. It’s our responsibility. The bank will use our money to its advantage and continue to pay the lowest rate possible until questioned. We moved the money electronically from within the same banking system from one location to another, and crazily enough, it now earns us much more interest!

Make a Game Plan

Set up a meeting at your bank, and be prepared with evidence of competitors offering higher rates on similar products. Your bank may be motivated to match it. A physical bank will not be able to compete with rates offered by online banks. You must compare apples to apples: find rates from banks similar to yours. If they are unwilling to raise rates on your savings, see if they will drop some of the service fees on accounts you have with them. If you are a long-time customer, they may be motivated to keep your business. Again, bring proof of lower fees with other banks.

Needless to say, conduct yourself as an ambassador of Christ. Be patient, listen well, and make sure you understand exactly what you are told.

If you are like most consumers, you like having checking and savings accounts at the same bank. Perhaps you are happy at your bank, but they are unwilling to meet the rates offered by competitors. Consider moving some of your money to take advantage of particular products that better meet your needs. Or consider a credit union. If you are unhappy with your current institution, then definitely shop around. Ask friends where they bank, and do some online research.

Compare Banks

When promotions are offered at other institutions, research the restrictions. Is the annual percentage yield (APY) worth moving your accounts? Here are a few other things to consider:

Compare CD Rates

Check out current CD promotions. Rates vary by terms—the length of time money must remain in the account. For example, a one-year term means the money must remain in the account for one year. This is a good option for locking away money you do not want or need to touch for a certain length of time. Early withdrawal will cost you money, so do not put all your savings into CDs. This can be very beneficial for impulse spenders, low-risk investors, or anyone with a time-specific savings goal. Currently, most CDs pay higher rates than savings or money market accounts, though they do not have the flexibility. Online rates exceed what physical banks can pay. You can ladder them by locking in rates for different periods of time. Here are two resources that might help:

You Snooze, You Lose

Don’t procrastinate. Get informed, and do what you can to protect and grow the money you are entrusted with managing. A wise steward will watch over his/her accounts, not because of fear or greed but because of a desire to maximize what has been provided in order to bless others and take care of future needs.

Be proactive. Proverbs 27:23–24a instructs: “Know well the condition of your flocks, and give attention to your herds, for riches do not last forever…” Flocks and herds were the riches and possessions of people in ancient days. Applying this today encourages you to diligently manage your savings for your good, the Kingdom, and those who will obtain the inheritance.

The Crown God Is Faithful devotional offers inspiring and practical Biblical wisdom. You can subscribe to receive daily devotionals that will help transform your finances and provide much-needed encouragement.

This article was originally published on The Christian Post on March 10, 2023.

Dear Chuck,

We are senior citizens. My wife thinks we need to start stocking up on some gold. I am not so sure; plus, I would not know how to do it without getting ripped off. Any advice?

Gold for the Golden Years

Dear Gold for the Golden Years,

The Bible speaks to a number of the issues raised by your question. Let’s look at the market for gold and then some advice.

Insurance or Investment

People buy gold for two primary reasons: insurance or investment. Typically, when the value of the dollar goes down, gold prices go up. When demand goes up, prices rise, and vice versa. Owning some gold helps as a hedge against the falling value of the dollar. Trouble happens when people rush in thinking they will get rich quickly or hastily liquidate other assets that are losing value in order to buy gold. This dangerous mindset leads people to make poor decisions about things they do not understand. As a result, many suffer significant losses. Truly, “The plans of the diligent lead surely to advantage, but everyone who is hasty comes surely to poverty.” (Proverbs 21:5 ESV)

Be On Your Guard against Gold Fever

History is filled with stories of people who got “gold fever” and were subsequently scammed. The Bre-X gold mining fraud occurred in 1997. An initial private offering at 30 cents per share jumped to more than $250 on the open market. J.P. Morgan, Lehman Brothers Inc., Fidelity Investments, Invesco Funds Group, and other companies jumped in, believing Egizio Bianchini, one of Canada’s top gold analysts, who said, “Bre-X has made one of the great gold discoveries of our generation.” What they did not know was that the project manager was tampering with core samples. All that glitters is not gold! He mysteriously fell to his death from a helicopter, Bre-X collapsed, and the shares became worthless. Here is more on the bizarre story.

Fast forward to today. Tyler Gallagher was recently CEO of Regal Assets, a company that let customers convert retirement accounts into metals like gold and silver. The company claimed that the program was a hedge against downturns in the stock market and inflation. Many who feared recession invested with Regal between 2020 and 2022. Most were in their 60s or 70s and trusted Gallagher with their life savings. He appeared very successful and talked the talk. They gave him their money but have yet to get the gold. Not only can the gold not be found, but neither can Gallagher. He has vanished. For more on this crazy story, read this.

Unfortunately, other scams exist, and seniors tend to be the most vulnerable.

Central Bank Holdings of Gold on the Rise

On January 27, 2023, the International Monetary Fund released a working paper entitled: “Gold as International Reserves: A Barbarous Relic No More?” Here are some notes:

Here is an excerpt from David McAlvany’s weekly commentary on February 8, 2023, titled “Why Are Central Banks Buying So Much Gold”: “For the global central bank community, gold maintains a 10% allocation of total reserves. That’s an average, and it’s a bit misleading because as an average, that includes the US, Germany, Italy, and France that keep a range of 58 to 66% of all their reserves in gold. . . . When you have slowing GDP, you have an increased interest in gold, the acquisition of it. When you have a weakening fiscal position in a country, the central bank says, ‘I think we should have some gold.’”

On February 1, 2023, the Financial Times featured a commentary on the increase of central bank gold holdings in 2022. Total demand across all categories came in at 4,741 tons—an increase of 18% from the previous year.

Invest, but Wisely

Gold bars (bullion) are sold by gram or ounce and should be stamped with purity, manufacturer, and weight. Bars that are investment quality must be at least 99.5% pure gold, especially if storing them in a gold IRA. Smaller-sized bars and coins offer greater liquidity and are common among those who own gold. Storage must be seriously considered, as well as insurance. Gold exchange-traded funds (ETFs) and mutual funds can be purchased and sold like other stocks. Many consider it the easiest and safest way to diversify one’s portfolio.

Avoid Craigslist, Facebook marketplace, dealers offering massive discounts, pawnshops, telemarketers, pushy salespeople, or dealers without a physical building. Avoid offers of free storage or delayed delivery. In addition:

Key Biblical Principles

To gain more wisdom and insight into how you can effectively steward God’s resources—both time and money—the Crown Stewardship Podcast can be valuable. You can subscribe for alerts of new episodes. I hope you find it beneficial.

This article was originally published on The Christian Post on March 3, 2023.

Dear Chuck,

I thought car prices were going to drop when chips reentered the market. I’m not seeing a drop where I live, and I really need to replace a vehicle. What should I do?

Waiting for a Deal on a Car

Dear Waiting for a Deal on a Car,

Most of us have never seen a car market that is so upside-down. Instead of negotiating for a price lower than the MSRP (Manufacturer’s Suggested Retail Price) for a new car, dealers are now setting the price they want above the MSRP. And in some cases, used cars are bringing more than what was paid for them new. Whew!

Let’s look at some key trends to help you with your question about timing.

Trends in the US Car Market

Car ownership is becoming more and more expensive due to the higher costs to insure and finance them. However, inflation and higher interest rates have resulted in fewer sales, so demand has dropped, which may bring prices down.

On February 13th, Bloomberg published an interesting article: “New Cars Are Only for the Rich Now as Automakers Rake in Profits.” Apparently, manufacturers are intentionally keeping inventories low and prices elevated to gain higher profits. Despite the fact that fewer cars were sold, Ford’s gross profit rose over 4%, and GM’s adjusted earnings grew by some $200 million. In the past, automakers typically carried 60–100 days of inventory. Today, they target half of that in order to lower overhead. Ford CFO John Lawler said he expects new-car prices to fall 5% in 2023. Nissan’s Wheeler predicted prices will drop toward “a more normal level.” Even so, customers who finance vehicles face average new-car payments of $777 or used-car payments of $544.

Cox Automotive reports:

Many people use tax refunds as an opportunity to buy a car. Unfortunately, the higher demand during refund season drives prices up. Avoid these mistakes when using a tax return to purchase a vehicle.

Hope for Lower Used-Car Prices

If demand surpasses supply, prices will stay high or grow higher. The average price of a new car in the US has jumped 30% since 2019 to $50,000. Used-car prices unexpectedly jumped 2.5% in January but are down 12.8% from 2022.

On February 17th, AutoNation reported that it expects used-car prices to drop. CEO Mike Manley said, “You are going to see improved balance and level of inventory. You’ll see it progressively more once you get out of the first quarter.”

Nerdwallet reported in January that used-car prices are dropping but at different rates. Pickups and compact cars have had the smallest price change since January 2022. SUVs and luxury cars have had the largest price drops. Supposedly, customers wishing to trade in their cars should expect lower values than last year. However, trade-ins can be helpful in negotiations since dealers need used cars.

The Manheim Index is becoming recognized by financial and economic analysts as the premier indicator of pricing trends in the used-vehicle market. Used-car prices are up nearly 40% over last year, with the average used-car price reaching $27,000.

Increased Auto Insurance

If car prices come down, auto insurance will cost more as insurers attempt to catch up with higher costs of repair parts, labor, and claims. There has been an increase in the frequency and severity of crashes, along with record levels of personal injury judgments and vehicle thefts. Rates are expected to rise 8.4% across the country this year, with the average cost of full-coverage insurance at $1,780 per year. However, rates vary by state. Progressive received approval to raise their rates by 19% in California for new and renewing policies. Facts that determine auto insurance rates include location, driving record, credit score, type of vehicle, and years of driving experience (teens are expensive).

Consider Your True Cost Per Mile

I drove through several used-car lots this past weekend and was still shocked at the prices. I’ve always tried to buy cars that will retain value. In 2009, I bought a low-mileage, one-owner, 2007 Toyota 4-Runner. It seemed expensive at the time, but in the 14 years I’ve owned it, the value has only decreased by about $5,000! To date, it has not required a single major repair either. So if I look at it from a cost-per-mile-of-ownership standpoint, I have driven about 100,000 miles for only $5,000, or about $.05/mile, apart from maintenance. I encourage you to do a similar calculation on any purchase you are considering to understand your true cost.

Pray about Your Next Car

Ask God to find you a car. Ask Him to provide one for you. He knows what you need, what you can afford, and what is available. Trust Him, and wait patiently but expectantly while you do your part in searching. When that prayer is answered, rejoice and give thanks. Sometimes, He provides in truly miraculous ways. A friend of mine was praying for a car he needed and was invited to play in a charity golf tournament. He was stunned when he hit a hole-in-one, the first in his life. The prize was a brand-new SUV, like the one he had been praying for. You never know what God may do.

I would like to invite you to join us at Crown’s 2023 Reunion. We plan to gather October 12–15 at Ridgecrest Conference Center near Asheville, North Carolina. For more details and registration, go to Crown.org/reunion.

This article was originally published on The Christian Post on February 24, 2023.