Dear Chuck,

Our house, cars, and credit card debt prevent us from giving to the church. We argue about this, but my husband wants to get out of debt first before we start giving. I think we are robbing God. Can you help unite us?

Divided Over Giving

Dear Divided Over Giving,

Thank you for your very sincere question. I believe there is hope for unity despite your different views. Like your husband, I held the same view for many years. I had good intentions and a plan to give generously—but only when we were not struggling financially.

Everyone Is Generous

For years, I was a very content charitable giver of 2.6% of our gross annual income. I believe this is close to the national average for American Christians. My wife wanted to give a minimum of 10% of our gross annual income, but I always told her that there was no way we could afford to do that. We were divided and stuck for many years.

A significant shift occurred in my thinking when a friend shared with me that everyone is generous. The challenge is what we prioritize. You see, I was giving generously to myself and my family. I was spending everything God entrusted to me on us.

Through the conviction of Scripture, a Crown Bible Study, and the encouragement of my wife, God changed my heart in 1999. We had been married for 21 years before we became united in our belief that giving to the Lord should become a priority. When my wife and I agreed to follow what God says we should do with money, He united us in our hearts and minds.

I remember telling my wife that if we increased our giving from 2.6% to 10%, that dramatic increase would require us to change our lifestyle. I said, “You realize this will change how much home we can buy, what we can afford to drive, and how we live, don’t you?” She replied, “Now you finally get it.”

We united around God’s truth that it truly is “more blessed to give than to receive” (Acts 20:35) and made giving to the Lord our top financial priority from one month to the next—before we got out of debt!

Giving is not a legal requirement to please God. It’s a tangible way for us to express our love to Him. It is our acknowledgement that He is first in our hearts, making it an act of worship. Giving is a privilege that we miss until we actually engage in it. But don’t try to convince your husband of this; pray and ask the Lord to do the conviction and bring you together.

What About Debt?

Since I don’t have a clear picture of your financial situation, I don’t want to assume that you can begin immediately giving to your church without careful planning. However, discuss with your husband what you might miss by waiting to get out of debt. Consider the missed opportunity of trusting God and seeing how He provides. By delaying the habit of giving regularly, you are missing out on the joy it brings. Plus, I have seen many times that when couples prioritize giving, it actually serves to help them reduce their debt more quickly.

When you have obligations to pay, giving can be extraordinarily challenging. Remember how Jesus pointed out the widow who gave her two small copper coins in Mark 12? She gave all she had, believing God would meet her needs. Those two coins—small to the world but large to her—demonstrated her complete dependence on the One who loved her.

Many find it easy to skip giving to God first. They choose to give what is left over after their own needs and desires have been met. I know I did. Even though debt must be paid, consider how you can cut spending elsewhere in order to give something to the Lord. Don’t do it reluctantly or under compulsion, but unite with your spouse and follow God. “God loves a cheerful giver” (2 Corinthians 9:7).

Consider giving an amount you know you can handle at first. It is ok to start small. The repeated action will establish the habit. By setting it aside ($1, $5, $10…), you will not spend it. Acknowledge the Lord while you are paying off your debts.

Trust Him to Unite Your Hearts

God sees and knows our struggles. He promises to meet our needs, but we have the responsibility of following His principles. I often hear from people who began taking steps of faith and giving first. God honored them, and somehow, someway, their debt was reduced in record time. Ask Him to help you live as a steward of all He provides. Ask Him to unite you and your spouse, so together you can find joy in managing things His way. Here are some great resources to help you:

If you’re burdened with credit card debt, consider reaching out to Christian Credit Counselors, a trusted partner of Crown. They are a valuable resource to help consolidate debt and get on the road to financial freedom so that you can become a more generous giver.

Dear Chuck,

We promised our children a theme park vacation this year, before I checked the prices. I am in shock. Should I back out or do it even though we can’t really afford it?

Frugal Family

Dear Frugal Family,

When I was a boy, my parents allowed me to take a trip to Disneyland with a family of six who were driving from Texas to California in a station wagon! It was one of those classic station wagons with a rear-facing seat that popped up in the storage area. To save money, we stayed in a tent in KOA campgrounds at each stop along the way. Even though it was a very low-budget trip in a crowded car that seemed to take forever to get there and back, it is a memory I will always cherish—not just the theme park but the entire experience.

We preferred other forms of family vacations with our children, so it’s been a long time since I’ve visited a theme park. However, since you made a promise, I suggest you do your best to keep it, unless your children change their minds. From what I’ve read, with some dedicated planning, you may be able to enjoy a budget-friendly trip.

Become Proactive Early

Disney raised ticket prices this year and went to dynamic pricing. This means prices will vary according to the date. So try to schedule the trip when prices dip, like during the hottest months. Another option is to go during school when rates are cheaper and there are fewer crowds. My wife, who helps me with these questions, found this article, which says Disney prices its parks based on the income of the top 20% of American households. It provides great information and charts for lodging, meals, and other fees.

Don’t get burned by buying discount tickets off eBay or Craigslist. They could be counterfeit. Deal with secure websites. The time you put into early planning could save you hundreds of dollars.

Stay Within Your Budget

Determine how much you can realistically afford for a vacation. Then resolve to stay within that amount or a little under, so you are prepared for any unexpected charges.

If you need some extra funds, work together as a family to exercise some cost-cutting and income-producing measures. Months before you make the trip, stop eating out, cut some streaming services, have a garage sale, or sell items on Facebook Marketplace. “Eat the pantry,” and prep frugal meals to save money. Working on it ahead of time will help you find deals, save money to pay cash, and ultimately find more pleasure in the trip! Bring your children into the effort to help them appreciate the commitment you have made to provide them with this special trip. Think about exploring our State and National Parks in the future. Taking your family into God’s creation can be a worshipful experience and far more affordable.

Money Saving Tips

Suggested websites for planning and more cost-saving suggestions:

Consider discussing alternatives with your children before you absolutely commit to a theme park vacation. Instead of theme parks, we joined a fishing club, and our now-adult boys look back on the time we spent out there as a favorite memory of their childhood. Trips to visit family were also a part of our vacations. These are important to help your children create more offline connections in an online world.

We were made to work and rest, so keep your own needs in mind as well. A lot of people I know return sunburned and exhausted after a theme park trip. So allow some time to recover when you get home. Be careful not to promise the children a trip that creates financial stress in the future!

Additional Reading:

Vacation Clubs, Timeshares, or None of the Above

Do you want more tools and tips on financial stewardship? Are you interested in receiving ministry updates from around the world? Sign up to receive the Crown Newsletter emails by using the form on the homepage at Crown.org.

This article was originally published on The Christian Post on May 23, 2025.

Dear Chuck,

I like buying luxury brands, but my husband couldn’t care less about the brand. He says he just wants quality. I argue we are getting both. Who is right?

Luxury Brands Are Quality

Dear Luxury Brands Are Quality,

This is a hard argument to mediate since I don’t have all of the information about your financial circumstances. I decided to research the “luxury brand” market and give you some perspective before I reply to who I think is right.

Who Is Buying Luxury Brands?

A 2020 article at Forbes describes luxury brands as exquisite, expensive, and exclusive. Marketers aim at the middle class and use celebrities to sell a lifestyle. To retain the scarcity of their products, some companies destroy their unsold items. This 2018 article reports how Burberry destroyed items to prevent them from being stolen or sold cheaply.

The market for luxury goods was estimated to be $254 billion in 2023 and is expected to reach $370 billion by 2030. An expanding global middle class is emerging across the world and is expected to tap into this market. Luxury items are now more accessible due to the adoption of digital channels.

One unidentified online source claims that two income-earning groups account for 75% of the purchase of luxury goods: those that earn less than $56,000 per year, with a net worth of less than $6,000, and those that earn $56,000–$168,000, with an average net worth of $104,000. The point of his post is that the majority of luxury brands are not purchased by the wealthy.

Most studies agree that the wealthy are not keeping luxury brands in business. They buy assets that grow in value or increase their cash flow—or both. They buy freedom, not status. They use money to create options, not to impress strangers.

The wealthy know that money should be working for them, not the other way around. Assets generate income while liabilities generate expenses. Assets pay; liabilities cost.

It’s been said that the poor buy stuff, the middle class buy liabilities, and the wealthy buy assets.

Rather than using common sense, waiting, and trusting God, some people are caught up in the need for luxury. It boils down to what you believe about money—how you use or steward God’s money.

The Appeal of Buying Luxury

Luxury marketing is aimed at aspirational shoppers: those who want to feel wealthier, cooler, or more successful than they can truly afford. A 2023 survey found that nearly 40% of Gen Z shoppers went into debt to purchase a luxury item. According to Bain and Company, about 75% of global luxury spending is from middle-income households. As previously mentioned, those with a high net worth account for a fraction of the sales.

The most common luxury purchases include designer clothing, handbags, jewelry, watches, and cars. Experts project that a third of the overall luxury brand market will be for apparel. However, there is a growing demand for “luxury experiences” over possessions. That, coupled with an awareness of sustainability and ethical practices, is impacting the purchase of certain items.

Luxury items are associated with strong emotions:

In the God Is Faithful Devotional, Larry Burkett wrote, “Greed has become such an accepted attitude that most major advertisements for luxury products are built around it. Many committed believers are convinced (often by other believers) that it is God’s absolute responsibility to make them wealthy and successful.”

What people will do to get luxury items:

We need to live our lives in such a way that we can meet our obligations as well as stand before God and give an account for our choices. To fully consider the costs of daily decisions, we must remember that eternity stretches before us and that our choices have long-lasting implications. We need to make sure our priorities for spending are greater than our desires.

Count the Cost before Spending Money

Freedom from the Grip

“Do not lay up for yourselves treasures on earth, where moth and rust destroy and

where thieves break in and steal, but lay up for yourselves treasures in heaven,

where neither moth nor rust destroys and where thieves do not break in and steal.

For where your treasure is, there your heart will be also.”

Matthew 6:19–21 ESV

Those who struggle with the desire for luxury items can be released from the emotional grip.

They need to recognize the stronghold, confess it, repent, and be grateful for all they have. They can ask God to help them be satisfied in Him and all that He provides. Meditating upon or memorizing a passage of Scripture helps bring things into focus.

My position is that you both have a valid point. It is possible to buy a luxury brand and also get quality. However, it is also possible to buy quality and get “luxury,” without overpaying for the brand name. I am, therefore, in support of your husband’s position. A friend of mine purchases the cheapest luggage at Walmart. He says he can replace it once every year for 20 years (if it breaks) and still spend less than a luxury brand piece of luggage. We need to remind ourselves that this is all temporal. Treasures in Heaven will be far more meaningful than a Louis Vuitton handbag.

Further Reading

Rationalizing a Luxury or Indulgence

Fake It Till You Make It” Lifestyle

Why Financing Is the New Layaway

Buying luxury goods can quickly lead to credit card debt. If you’re burdened with credit card debt, consider reaching out to Christian Credit Counselors, a trusted partner of Crown. They are a valuable resource to help consolidate debt and get on the road to financial freedom.

This article was originally published on The Christian Post on May 16, 2025.

Dear Chuck,

We need to purchase a car on a tight budget. We’d like to buy a dependable used one, but we hear that parts are going up due to tariffs. I know you like to purchase used, but is that still our best option?

Buying a Car on a Budget

Dear Buying a Car on a Budget,

A car purchase has become a major life decision and can lead to a cascade of financial problems if the car is unreliable or it puts stress on your budget. Like you, many are concerned about used (and new) car prices and how to afford the best options.

The key is finding balanced information that doesn’t exaggerate the potential impact of tariffs. Deals are out there if you have the discipline to exercise patience, do your homework, and stay within your budget.

A Personal Experience

Even with the best of plans, it does not always go well. I recently did the research for one of our sons who needed a pickup for his work. Despite all of my best efforts at finding the perfect used model for him and his wife, it has consistently given them mechanical problems. Sometimes buying new is the best option, so don’t rule it out, depending on your budget.

Car Market in 2025

CarEdge.com reports that the average price of a used car this month is $25,128. The spring car buying season, combined with market uncertainty, may push prices higher for a while. Tariffs, supply chain disruptions, inventory, and interest rates are all factors. If new car prices go up, expect used ones to do the same. As for now, it’s a used car seller’s market.

Value in Timing

I do a lot of research before making a purchase, comparing sales at dealerships, Cargurus.com, and Facebook Marketplace. Timing, as reported by U.S. News, is important:

Sometimes, the best time to buy a used vehicle is after big sales events. Wait a few days for trade-ins to move onto the dealers’ used car lots. Those who sell privately may wait until after they have purchased a new one. Be careful buying after a flood or natural disaster. I search for one-owner or certified pre-owned cars that have maintenance records and low mileage. I always use CarFax to check the history and never buy a car that has been to auction or has a rebuilt title. A rebuilt title means it was declared totaled by an insurance company at some point in its history.

Value not Vanity

Buy cars for value, not vanity. Mark Zuckerberg (Meta), Larry Page (Google), and Jeff Bezos (Amazon) drove unassuming cars for years: Honda Fit, Toyota Prius, and Honda Accord. Warren Buffett drives a 2017 Cadillac sedan. The wealthy realize that most cars depreciate in value and prefer to put their money in appreciating assets. Understated vehicles don’t attract attention. Reliability, good gas mileage, and one that does not attract a lot of attention is preferred. Plus, insurance can be less expensive.

A study from Experian Automotive showed that 61% of households earning more than $250,000 annually don’t own luxury brand cars. They choose to drive mainstream brands or modestly priced luxury vehicles that coincide with their values and needs.

Value in Prayer

Ask God to provide. He knows exactly what you need and when you need it. One friend of mine was in need of a vehicle, and during his time of waiting on the Lord, he was invited to a charity golf tournament. For the first time in his life, he hit a hole-in-one while playing golf that day. The prize was a brand new car. He knew in his heart that the Lord provided in the most unexpected way!

Be patient while keeping a lookout. Let others know you are in the market. They may know someone who wants to replace a vehicle.

If any of you lacks wisdom, let him ask God,

who gives generously to all without reproach, and it will be given him.

But let him ask in faith, with no doubting…

(James 1:5–6a ESV)

Articles to check out for more information:

Do you want more tools and tips on financial stewardship? Are you interested in receiving ministry updates from around the world? Sign up to receive the Crown Newsletter emails by using the form on the homepage at Crown.org.

This article was originally published on The Christian Post on May 9, 2025.

Dear Chuck,

My fiancé and I hope to marry in November. Our parents are not in a position to help financially. I’ve felt anger and sorrow about that, but I want to have a great wedding without spending lots of money. Haven’t you written about ways to save money on weddings?

Wedding Without Financial Stress

Dear Wedding Without Financial Stress,

No need to be worried or upset about your family’s inability to help you pay for a wedding. In fact, you can view it as a blessing.

My wife and I were married long before cell phones, Instagram, and Pinterest. We had a simple wedding and honeymoon, and our first apartment was furnished with used furniture. We didn’t care! We weren’t comparing ourselves to others. We were happy with what we had and stayed busy working and going to school.

Weddings Can Get Expensive

It’s a different world today! According to The Knot Real Weddings Study, 53% of couples spent more on getting married than they planned, by an average of $7,347. Since the average cost is around $33,000, going over-budget would bump that figure to $40,000!

Weddings have become a big business. Social media has created desires and expectations for everything—from engagement rings to the wedding cake and everything in between. Brides are influenced by Pinterest and Instagram, magazines, blogs, apps, and Google searches. Young girls imagine, dream, and plan their weddings. They carry those dreams into adulthood without asking God for wisdom or seeking the advice of those older and wiser.

Suppose the wedding and reception last four hours. That means the average couple spends $10,000 an hour for the event. Granted, that’s not a worry for some people, but for others, it’s a LOT of money! Some (usually parents) recognize that money could be used for the down payment on a house, a newer car, career/skill training, or starting a business.

Keep It in Perspective

Your wedding is a significant moment in time, but it is just one day in your life. Once married, you will share many days together, Lord willing. While barns, beaches, and destination weddings make great social media posts, there is beauty in church weddings, where couples are celebrated by the congregation in a setting conducive to worship. Some churches have fellowship halls for a reception, an outdoor pavilion, or space to set up a tent. I’ve officiated a home wedding and one in a park. Both were beautiful, and the couples were spared great expense. Receptions held in venues not typically used for weddings can also be less expensive. Just make sure you understand the rules for catering, and read the contract in its entirety before signing.

Focus on the Marriage, Not Just the Wedding

My advice is to renew your heart and mind with an eternal perspective of your wedding day. Choose simplicity over stress and financial margin over debt. It’s a matter of stepping back in order to think realistically. Spend focused time in prayer, make peace with what you can afford, give thanks for your future husband, and ask the Lord to be at the center of all your plans. Aim to make your ceremony a time to worship Him as you dedicate your lives to one another.

Do

Don’t

Money Saving Tips

Begin your marriage using money wisely. It is crucial for your future financial success. I highly recommend that couples go through our Money Dates or Money Life Personal Finance Study. These will help you set your course, enabling you to align goals and have a plan to achieve them from day one.

I hope more churches will encourage ceremonies to be held on their property. Forming a committee to encourage and support church weddings at lower costs would be a blessing. If you have not asked your church about this, possibly send them this article.

More Information

If you’re entering marriage with credit card debt, consider reaching out to Christian Credit Counselors, a trusted partner of Crown. They are a valuable resource to help consolidate debt and get on the road to financial freedom.

This article was originally published on The Christian Post on May 2, 2025

Dear Chuck,

My parents are extremely fearful about the future of Social Security benefits. How can I help them with their concerns?

Fearful About Social Security

Dear Fearful About Social Security,

A recent Gallup report reveals that 52% of Americans worry about the Social Security (SS) system. It has been at the top of the minds of millions who are approaching or in their retirement years. Although this is not a new fear, it has been making headlines of late.

The Department of Governmental Efficiency (DOGE), in an effort to eradicate mistakes and fraud at the agency, has caused quite a stir among SS recipients. Political opponents are seizing the opportunity to create fear and unrest through the airwaves. As a result, many people are being misled by presumptions.

Some fear that cost-cutting measures will impact their benefits. The reality of it is that those who are receiving payments fraudulently should be afraid. Those who received overpayments and never reported them should expect repercussions. But what about the unrealistic fears that people are feeling?

Stirring the Pot

Former SSA commissioner Martin O’Malley, interviewed on CNBC, made comments which would indeed be unsettling if one didn’t recognize that his presumptions were opinions, not facts. He stated:

CNBC also referenced comments made by Jill Hornick, a union official at the American Federation of Government Employees Local 1395, representing SS offices in Illinois. She noted that “it will take a while for the effects to be felt, but they’re coming,” predicting that changes in SS will be “far worse” than the Medicaid planned cuts. In addition, she thinks processing new claims could be delayed due to an understaffed workforce.

Both people based their negative response to SS changes on presumptions. According to James 4:14, these types of statements are misleading, for no one knows “what tomorrow will bring.”

Facts Can Reduce Fear

What Now?

I believe it was Milton Friedman who said we can always expect the government to pay people their benefits, but the purchasing power of the benefits when received cannot be guaranteed. This is a very good point, since inflation can lower the purchasing power of future retirement income.

As Christians, we should assume the responsibility ourselves for saving and investing by living and planning as if Social Security will not be there. Prior to 1940, Americans did not receive Social Security benefits. President Roosevelt (FDR) signed the Social Security Act in 1935. The collection of taxes began in January 1937, and monthly payments started three years later.

It is better to rely on the Lord and follow His precepts.

“Wisdom is good with an inheritance, an advantage to those who see the sun. For the protection of wisdom is like the protection of money, and the advantage of knowledge is that wisdom preserves the life of him who has it.”

(Ecclesiastes 7:11–12 ESV)

“Moreover, it is required of stewards that they be found faithful.”

(1 Corinthians 4:2 ESV)

Live Contrary to the Way the Government Does

Our government has low or no savings and excessive debts, but so do many Americans. This should increase our motivation to do the opposite. Do not run up unnecessary debt. This requires sacrifice and self-control.

“Owe no one anything, except to love each other, for the one who loves another has fulfilled the law.”

(Romans 13:8 ESV)

“The rich rules over the poor, and the borrower is the slave of the lender.”

(Proverbs 22:7 ESV, emphasis mine)

Many people carry excessive credit card debt and find themselves trapped in a cycle of borrowing. Anyone experiencing this burden should get in touch with our friends at Christian Credit Counselors. They have helped hundreds of thousands of families experience freedom from debt.

Do Not Fear

Assure your parents that no one knows what tomorrow holds. So why waste time and emotions concerned about changes in Social Security? Instead, live frugally, give generously, save regularly, and invest wisely. Put your hope in the Lord, not man or government programs.

“Therefore do not be anxious about tomorrow, for tomorrow will be anxious for itself. Sufficient for the day is its own trouble.”

(Matthew 6:34 ESV)

“Trust in the Lord with all your heart, and do not lean on your own understanding.

In all your ways acknowledge him, and he will make straight your paths.”

(Proverbs 3:5–6 ESV)

I’d like to invite you and your parents to join a free Crown Bible study on the YouVersion app. We have several devotionals regarding money and stewardship that will provide encouragement by bringing God’s Word into your daily life.

This article was originally published on The Christian Post on April 18, 2025.

Dear Chuck,

With the new Trump tariff wars, I fear the stock market will tank, and my retirement savings will be gone. Are you advising people to get out of the market during this downturn?

Terrified of the Tariffs

Dear Terrified of the Tariffs,

I can’t give you investment advice; however, I can address some issues that are expressed or implied in your question. My intent is to offer you some Biblical principles to avoid the most common mistake any investor makes, which is to buy high and sell low.

Perspective on the Market

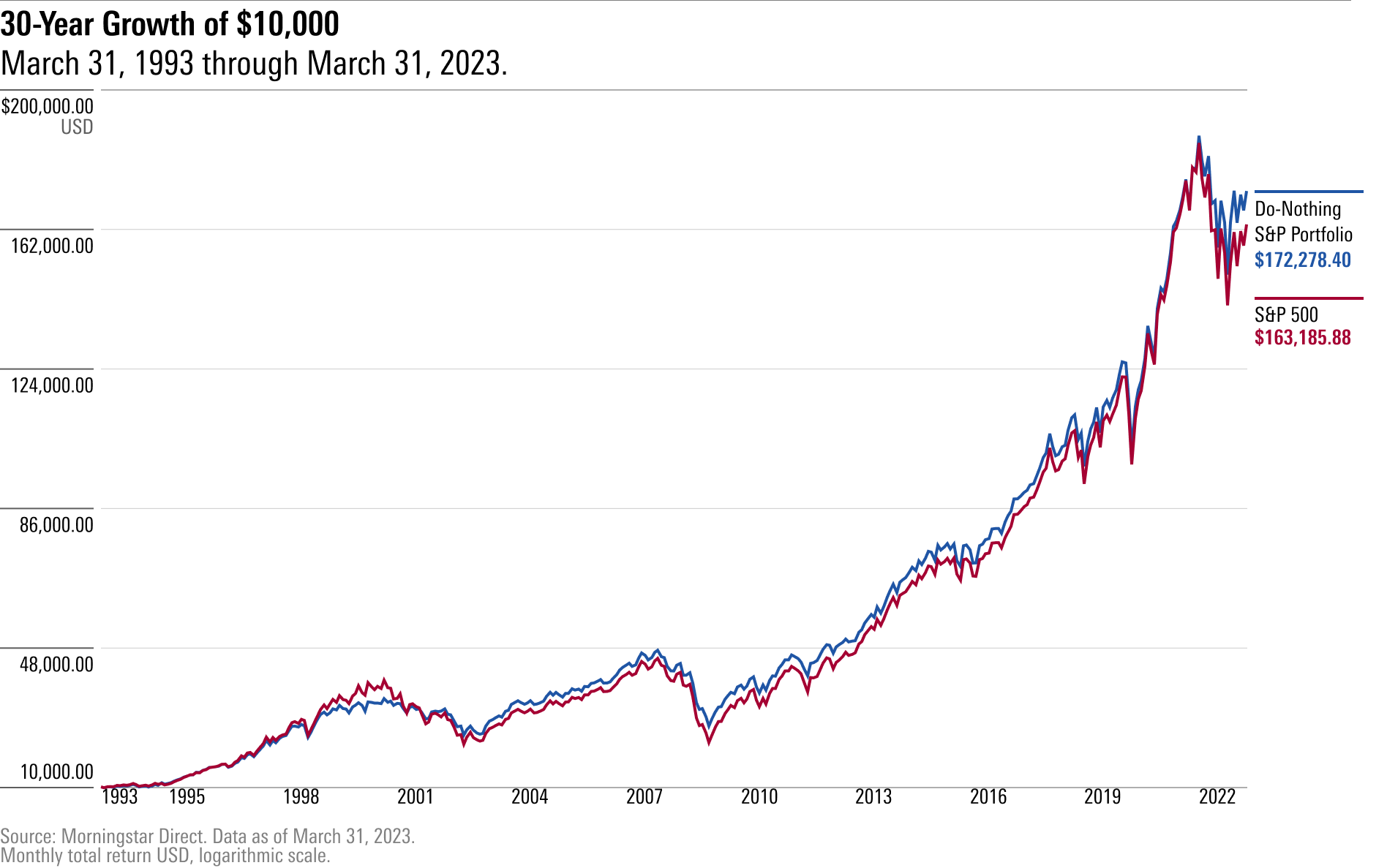

The year 2025 is shaping up to be one of the most volatile in recent history. We have seen declines in the markets year-to-date, with more declines possible. But remember, the S&P is still up more than 100% over the last five years, a historical bull run. While some panic, for many, it is an opportunity. It helps to think of it like a roller coaster that has ups and downs but consistently grows over time, increasing in value.

In a recent interview, Warren Buffett said something to the effect that if the value of your house went down, would you immediately decide to sell it? Surely not! Wouldn’t you continue to live there and wait to sell until the value increased? Owning stock in a company is very similar. Forget about the ups and downs of the stock market price.

“Some people should not own stocks at all because they get too upset with price fluctuations. If you’re going to do dumb things because a stock goes down, you shouldn’t own a stock at all.” –Warren Buffett

Historically, recessions typically last an average of 13–18 months, and then growth returns. The key is to be able to endure the fluctuations in your stock portfolio without making a reactionary decision to liquidate when the prices are at their worst. Obviously, the stocks you own should be evaluated consistently to factor in market changes, poor management, and other forces that could impact long-term value.

Age-Adjusted Risk

Investments should be analyzed by risk as you age. If they have historically weathered the storms, adjustments may be unnecessary. Most professional advisors stress the importance of reducing risk prior to and after retirement. In addition, the Bible stresses the importance of diversification, which is another way to reduce risk.

“Give a portion to seven, or even to eight, for you do not know what disaster may happen on earth.” (Ecclesiastes 11:2, ESV)

Seek many counselors. Think of investing like planting a tree. It needs decades to grow. Digging it up and moving it every time there is a storm will interrupt its opportunity to grow.

Buy Low, Sell High

Markets move on sentiment or emotion. People take action when they are fearful or greedy. The goal is to avoid following the crowd in the wrong direction. Like someone yelling fire in a theater, many may be crushed by the panic to escape instead of waiting to see if there really is a fire.

John Templeton famously said the best time to buy stocks is at the point of peak pessimism and fear, and the best time to sell stocks is at the point of peak optimism.

Buffet says that the poem If by Rudyard Kipling is good to ponder during market turmoil. It is a reminder to avoid panic in the midst of market fluctuations, to ignore the fears created by the “what-ifs,” and to patiently wait things out.

Dealing with Fear

We are called to live one day at a time. Only our heavenly Father knows the future. When we try to enter His realm, we can be overcome with fear and anxiety. That’s why Jesus’ instruction in Matthew 6:33–34 is so important:

“But seek first the kingdom of God and his righteousness, and all these things will be added to you. Therefore do not be anxious about tomorrow, for tomorrow will be anxious for itself. Sufficient for the day is its own trouble.” (ESV)

“He will give them to you if you give him first place in your life and live as he wants you to. So don’t be anxious about tomorrow. God will take care of your tomorrow too. Live one day at a time.” (TLB)

I’d like to invite you to join a free Crown Bible study on the YouVersion app. We have several devotionals regarding money and stewardship that will provide encouragement by bringing God’s Word into your daily life.

This article was originally published on The Christian Post on April 11, 2025

Dear Chuck,

I have plenty of money but no peace. What is there not to worry about right now? I have generalized stress about the economy, political divisions, cultural influences on my kids, wars, hatred… the list is long. How can I escape this spiral of non-stop worrying?

Anxious About Everything

Dear Anxious About Everything,

Thank you for your honesty. There is plenty to worry about through the lens that you are viewing the world.

We’re witnessing societal unrest (turmoil) from people whose meaning and purpose in life are linked to current events. Pessimism is rampant. Journalists, who get paid by the size of their viewership, are filling the airwaves with doom and gloom, which is creating fear, uncertainty, and anger. If you watch TV, read the news, or listen to podcasts, you will see and hear people who are anxious, devoid of joy, filled with fear, and possibly even paranoid. Their emotions are spilling over into acts of hatred and violence.

Grumbling

Like the Israelites who were rescued from slavery in Egypt, many within our population are fixated on what they perceive to be their losses. Their grumbling outweighs their gratitude.

“Now the rabble (disorderly mob) that was among them had a strong craving. And the people of Israel also wept again and said, ’Oh that we had meat to eat! We remember the fish we ate in Egypt that cost nothing, the cucumbers, the melons, the leeks, the onions, and the garlic. But now our strength is dried up, and there is nothing at all but this manna to look at.’”

(Numbers 11:4–6 ESV, parentheses mine)

Seeing Through God’s Lens

Rather than dwelling on God’s miraculous rescue and His abundant provision, they chose to focus on what they missed. Instead of giving thanks for the day’s gift, they were trapped in discontentment and projecting a future of deprivation.

Regardless of the actions of any government, believers must place their hope and dependence on God. Filled with the Spirit of God, we can be strong and courageous, knowing that the Lord our God is with us. Our hope is not in this world but in the world to come.

We may be tested and even suffer financially. Or we may prosper! Only God knows the future. Our responsibility is to obediently follow Him and live in such a way that we reflect the source of our hope to the anxious world that has no hope.

As the Apostle Paul said, “I have learned in whatever situation I am to be content. I know how to be brought low, and I know how to abound. In any and every circumstance, I have learned the secret of facing plenty and hunger, abundance and need. I can do all things through him who strengthens me.” (Philippians 4:11b–13 ESV)

The writer of Hebrews said, “Keep your life free from love of money, and be content with what you have, for he has said, ’I will never leave you nor forsake you.’” (13:5 ESV) The implication is that money is temporary, but our relationship with God is eternal.

Biblical Solutions to Fight Off Anxiety

We have so much here to be thankful for. Yet, without an attitude of gratitude, many bring mental suffering upon themselves and others. I conclude that they are:

Is it productive to worry about possible financial scenarios? No! Worry is like a rocking chair; you are constantly expending energy but getting nowhere.

Instead, follow God’s financial principles and do your part in diligently preparing as He directs. Do not depend on the government for your financial security. Do not place your identity in a job or company. Do not spend more than you make; make necessary sacrifices to get your house in order.

Direct any spun-up emotion into productive activities so that you can “laugh at the days to come,” like it says in Proverbs 31:25b. With your confidence placed fully in the Lord, you can ask Him for wisdom to protect your home and business financially.

Take These Actions Every Day

Pray: John 15:7

Trust: Proverbs 3:5–6

Depend on God: Philippians 4:19

Walk by the Spirit: Galatians 5:16–26

Suffer well: Romans 5:1–5

Give thanks: 1 Thessalonians 5:16–18

Prepare to defend your hope: 1 Peter 3:14–17

Rest Your Mind

God will give each of us problems that money cannot solve, but He will also give us true riches that money cannot buy. We can be anxious about our problems, or we can be joyful about all that we do have, even when we are suffering.

“You keep him in perfect peace whose mind is stayed on you, because he trusts in you.”

(Isaiah 26:3 ESV)

“Count it all joy, my brothers, when you meet trials of various kinds, for you know that the testing of your faith produces steadfastness. And let steadfastness have its full effect, that you may be perfect and complete, lacking in nothing.”

(James 1:2-4 ESV)

Are you interested in receiving encouraging ministry updates from around the world? Do you want more tools and tips on financial stewardship? Sign up to receive the Crown Newsletter emails by using the form on the homepage at Crown.org.

This article was originally published on The Christian Post on April 4, 2025

Dear Chuck,

My husband and I have lived frugally since getting married ten years ago. We’ve been paying off student loans, cars, and credit card debt. I’d like to use our tax refund for a vacation, but my husband insists that we pay off more debt.

Divided Over Tax Refund

Dear Divided Over Tax Refund,

Congratulations on the perseverance demonstrated by paying down your debt. I agree it can get tiring, old, and even depressing. That is why it is essential that you focus on the goal and give thanks for a husband who cares enough to protect your financial situation. At the same time, there needs to be room for some celebration that meets both of your objectives.

Affordable Celebrations

Find ways to celebrate how far you’ve come without blowing through the refund. Maybe your dream vacation can be postponed until more debt is reduced. In the meantime, consider alternative ways that will not cost money but will bring you joy together. Time spent in nature hiking, biking, and picnicking can be rejuvenating physically and emotionally. I have friends who love to hike and bike in the Smoky Mountains. Others take hammocks, books, and a picnic to relax. Perhaps you prefer pickleball, tennis, public gardens, museums, camping, etc.

Avoid Going Crazy

Unfortunately, many people fail to realize the importance of stewarding their tax refund. An article at Credit Karma says Americans blow their refunds like it’s free money. Results of a study conducted on their behalf revealed that by this time last year, “more than a quarter reported they already used or plan to use their refund to splurge on things they otherwise wouldn’t buy such as clothing and accessories (45%), electronics (40%) and shoes (37%). This trend was more pronounced among younger generations with 39% of Gen Z and 36% of millennials admitting plans to splurge.”

Here are just a few ways people (in debt) foolishly spend their refunds:

Good Stewardship of Your Refund

These are my three suggestions regarding tax refunds for people in debt:

Stay United

Whether debt is an issue or not, this article explains how to put a refund to good use. More important than what you do with the money is how you work to stay united as a couple. A tax refund is money the government owes you. It is not a gift or financial windfall. It is money

you worked for, so wisely put it to work for you. Your husband may already have a plan to maximize your return. Be honest with each other, consider all your options, pray, and ask the Lord to bring you to an agreement. I hope the two of you will ask the Lord to bless your efforts and unite your hearts with common goals. Hopefully, these ideas are a starting point for your unified approach.

Commit your work to the Lord, and your plans will be established.

Proverbs 16:3 ESV

If you need extra help in making a plan to pay off credit card debt, consider reaching out to Christian Credit Counselors, a trusted partner of Crown. They are a valuable resource to help consolidate debt and get on the road to financial freedom.

This article was originally published on The Christian Post on March 28, 2025.

Dear Chuck,

We have a young child with disabilities. Can you advise us on how to prepare financially for her care?

Special Care Needed

Dear Special Care Needed,

For the many friends that I have who love and care for their child (or children) with special needs, there are additional financial, emotional, and, at times, spiritual burdens. Some have questioned God, and some have been able to rejoice that they were chosen to be faithful stewards of God’s very special, unique, and marvelous creations. I have been blessed to hear their testimonies that celebrate the faithfulness of God to bless their families in ways that would have never happened without the child God entrusted to their care. I am so glad you are preparing financially for their long-term needs.

Your situation is far from uncommon. I researched the prevalence of people living with disabilities in the US. The research will provide some helpful context.

Making Plans

It is important to make financial plans so you can take care of the entire family while also setting reasonable goals to ensure your child gets quality care. It is equally important that you have people to call on and resources to handle the additional demands on your life.

According to the National Institutes of Health, the yearly cost of raising a child with disabilities in 2001 was $8,742. The estimate for 2025 is nearly $16,000. According to a 2020 study, a household containing an adult with a disability that limits their ability to work requires an average of 28% more income.

Raising a child with autism spectrum disorder can cost at least twice as much as raising a typically developing child. M&L Special Needs Planning reports that lifetime expenses for these children can reach $3.2 million, depending on circumstances. In some cases, government assistance is available.

Don’t allow these estimates and large numbers to overwhelm you. God is our Provider. He is faithful to meet the challenges and needs of each day.

Financial Challenges

Best Practices

Discover Resources and Financial Aid

An ABLE account is a savings and/or investment option for people with disabilities who qualify. It falls under Section 529A of the Internal Revenue Service tax code. The ABLE Act allows a person whose disability began before age 26 to save money in the ABLE account without affecting most federally funded benefits based on need. (Note that on January 1, 2026, the age of ABLE eligibility will be expanded to include people with a disability that began before age 46.) The money in the account may be used to pay for qualified disability expenses (QDEs). Any growth in the account from investments is not taxed and does not count as income if the funds are used for QDEs.

These accounts:

SSI provides monthly payments to people with disabilities and older adults who have little or no income or resources. Payments are subject to multiple factors but should be a consideration.

If your child with a disability is uninsured, needs additional services, or needs wrap-around Medicaid coverage to help with finances and uncovered services, your child probably needs a Medicaid waiver or program. These programs waive one or more Medicaid rules in order to extend eligibility and/or services to children. For children, the most common rule to be waived is the way income is calculated, meaning the program is based on the child’s income instead of the family’s income. Since most children don’t have any income, these programs allow the vast majority of children to qualify, regardless of how much money their parents make.

Your Local Church

Reach out to your local church. If it does not have a program serving families like yours, consider initiating the conversation to educate and make the need known. Request help from trustworthy friends and community programs. Joni & Friends has been serving people with disabilities since 1979. They offer practical help along with the saving love of Jesus.

Be Strong and Persevere

Raising a special child takes humility, strength of character, and dependence on others, primarily the Lord. He entrusted you with the child and will strengthen you for the days ahead. When you don’t know what to do, run to Him, remembering the words from James 1:5:

If any of you lacks wisdom, let him ask God, who gives generously to all without reproach, and it will be given him. (ESV)

There will be days you will have to depend on Him for mercy and strength to carry on. He promises to supply your needs. Despite the challenges you may face, know that He is with you, He loves you, and He will not forsake you.

Not only that, but we rejoice in our sufferings, knowing that suffering produces endurance, and endurance produces character, and character produces hope, and hope does not put us to shame, because God’s love has been poured into our hearts through the Holy Spirit who has been given to us. (Romans 5:3–5 ESV)

My hope is that these few directives will provide you with direction, encouragement, and helpful resources. Thank you for your question. Blessings to you and your special family.

I’d like to invite you to join a free Crown Bible study on the YouVersion app. We have several devotionals regarding money and stewardship that will provide encouragement by bringing God’s Word into your daily life.

This article was originally published on The Christian Post on March 21, 2025.